Stablecoins have been high on the agenda at payments conferences and in boardrooms since 2025, not because they will replace cards or bank transfers anytime soon, but because they are beginning to change how cross-border payments move and how treasuries manage settlement.

What Are Stablecoins?

Stablecoins are digital assets designed to maintain a stable value, typically pegged to a fiat currency such as the US dollar. Unlike cryptocurrencies such as Bitcoin or Ethereum, whose prices fluctuate based on market dynamics, stablecoins aim to hold a steady value by being backed by a pool of reserve assets (e.g. cash or short-term government securities). They also differ from central bank digital currencies (CBDCs), which are issued and backed by central banks and carry legal tender status. Stablecoins are typically issued by private entities and operate on public blockchains or distributed ledger systems. In this way, they combine the stability of fiat money and the programmability of digital assets.

Why Is Interest in Stablecoins Accelerating Now?

Interest in stablecoins has accelerated in recent years due to regulatory clarity and advantages in payment infrastructure. According to Visa Onchain Analytics, total stablecoin transaction volume between Q2 2024 and Q2 2025 reaches $33 trillion. While this figure includes non-payment activity such as smart contract interactions, Visa’s adjusted figures show payment-related stablecoin volumes growing from $5.99 trillion in 2024 to $11.1 trillion in 2025, an 85% year-on-year increase.

Regulation has played an important role. In the US, the GENIUS Act (enacted July 18, 2025) introduced clearer standards around reserve requirements and disclosures for issuers. In Europe, MiCA (enacted in 2023) created unified rules for regulating crypto-assets and crypto-asset service providers. Together, these frameworks reduce legal uncertainty and make it more feasible for banks and global payment providers to engage with stablecoins at scale.

Stablecoins can also address persistent inefficiencies in traditional payment infrastructure, particularly around cross-border settlement complexities and costly correspondent banking chains. With 24/7 availabilityand programmable transfers, stablecoins reduce operational friction and create economic incentives for adoption even without widespread consumer usage.

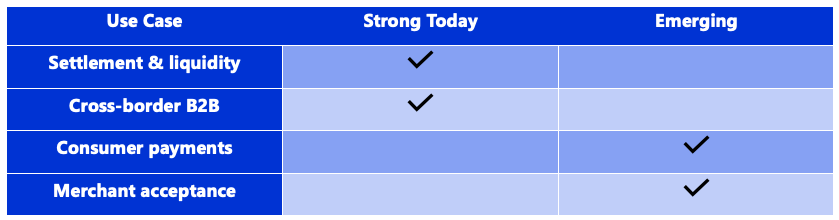

What the Stablecoin Market Looks Like Today

The stablecoin market is highly concentrated. According to research by JPMorgan, US dollar–pegged stablecoins account for approximately 99% of global supply. Tether (USDT) and Circle (USDC) dominate the ecosystem, together representing the majority of outstanding supply and transaction activity. This concentration suggests trust and risk are concentrated at the issuer level. In the meantime, new entrants and non-USD denominated stablecoins, such as euro-pegged tokens,are beginning to gain traction. Regulatory frameworks such as MiCA maygradually support diversification.

The most mature stablecoin use cases are cross-border applications and treasury operations such as institutional fund transfers and balance management. For example, JP Morgan’s Kinexys network (formerly Onyx) enables tokenized assets to be transferred and settled across borders with greater speed and transparency. Swift has announced plans to integrate a blockchain-based shared ledger following successful digital asset interoperability trials. Stripe’s $1.1billion acquisition of Bridge in 2025 further indicates demand for stablecoins as settlement infrastructure, enabling platforms to move value without managing on-chain complexity directly. In these contexts, stablecoins are less about consumer experience and more about operational efficiency.

Consumer trust is also emerging as a key factor for adoption growth. Research from FIS Global indicates that while nearly 75% of consumers would consider using stablecoins if offered by their bank, many continue to cite concerns about unregulated entities as a key barrier today.

Examples include PayPal’s Xoom platform offering zero-fee remittances using PYUSD, Kraken’s P2P payments app enabling transfers in crypto and fiat, and Visa’s pilot of stablecoin payouts through Visa Direct in partnership with infrastructure providers such as BVNK. These use cases demonstrate that stablecoins can function as reliable payment instruments for cross-border and peer-to-peer (P2P) transfers.

Key Challenges

Despite growing momentum, stablecoins face substantial challenges:

- Confidence in reserves and redemption is critical. Any perceived weakness could trigger sudden outflows.

- Regulatory fragmentation persists across jurisdictions, which may increase complexity for cross-border use cases.

- Integration with legacy systems remains costly, particularly for retail use cases. Widespread adoption will depend on scalable and reliable on- and off-ramp infrastructure.

Who Wins

Stablecoin issuers such as Tether and Circle benefit from growing transaction volume and deeper integration into mainstream financial flows. Yet, infrastructure providers like BVNK and Bridge are emerging as critical enablers, partnering with major payment platforms to embed stablecoins into existing offerings. Since they control integration, compliance, custody, and liquidity, these providers may capture more economic value than the issuers themselves.

Meanwhile, remittance providers historically reliant on FX spreads may face margin pressure. Financial institutions that delay investing in stablecoin-compatible infrastructure will risk falling behind, as clients increasingly expect faster settlement, lower cost, and more transparency.

Interested in discussing stablecoins and how these emerging trends could affect your organization?

We would be happy to continue the conversation.

Samee Zafar, CEO

samee.zafar@edgardunn.com

Tue To, Head of Fintech

tue.to@edgardunn.com

Davide Villa, Manager

davide.villa@edgardunn.com

Sam Crawford, Analyst

sam.crawford@edgardunn.com

Edgar, Dunn & Company is an independent and global strategy consulting firm specialising in payments and digital financial services. The firm was founded on two fundamental principles of client service: provide deep expertise that enhances clients’ perspectives and deliver actionable advice that enables clients to create measurable, sustainable change in their organisations. Our team is composed of experienced professionals who take a highly pragmatic approach to client issues and deliver analysis that is solidly grounded by experience and know-how. We provide both strategic advice and the business services required to translate that advice into action. Our team is made up of consultants with varied nationalities. We have native speakers covering key markets around the world.

%20(1).webp)

%20(1).webp)

.webp)

.webp)