.webp)

Agentic commerce is poised to bring profound changes to online travel agents (OTAs) for leisure travel, with AI-driven agents set to automate search, comparison, booking, and personalisation for travellers, fundamentally reshaping both user experience and operating models. In this article we look at the potential implications of agentic commerce on payment acceptance for OTAs.

AI agents are expected to increasingly act on behalf of travellers, autonomously searching, comparing, and booking hotels, flights, and packages using natural conversation rather than keywords or web navigation. This shift will reduce the relevance of traditional checkout pages, moving transactions into conversational interfaces, and may erode the competitive edge of OTAs that rely on web design, or the traditional sales funnel optimisation.

Today, or at least before agentic commerce becomes mainstream, travellers book directly with the travel supplier or via an OTA. An OTA serves as an intermediary between travellers and travel suppliers (such as airlines, hotels, etc.), handling bookings and payment flows either under the “reseller” model1 or the “pass-through” model2.

Under the reseller model, the OTA charges the traveller directly for the full value of the booking, acting as the merchant of record (MoR), and processes the payment. Then, the OTA pays each travel supplier separately, often using virtual credit cards in the name of the travel agent or other digital payment methods. In this model OTA assumes responsibility for:

- Collecting customer payments in various currencies and local payment methods

- Enforcing customer authentication and fraud prevention

- Managing the entire payment lifecycle, including chargebacks and refunds, as well as payouts to travel suppliers

- Providing booking confirmations and receipts to the customer

This approach allows the OTA to offer bundled packages (i.e., multiple services in a single basket) and control pricing; it also means the OTA bears full payment liability and must comply with applicable payment regulations, such as Strong Customer Authentication (SCA).

In the pass-through model, the OTA passes the traveller’s payment information to each travel supplier, and it is the travel supplier (and not the OTA) who acts as the MoR and processes the payment directly. The OTA then typically receives a commission for the booking. In the agency model:

- The OTA avoids direct payment liability and fraud risk

- The travel supplier manages the entire payments lifecycle

- The customer is likely to see individual charges from multiple travel suppliers

The Agentic Commerce Ecosystem

To dive into the impact of agentic commerce, first we need to understand that there are three types of foundational models that are shaping this new ecosystem:

- Business-to-Agent: where businesses (merchants) interact directly with AI agents representing travellers, tailoring their offerings to algorithmic decision-making. For example, an OTA provides APIs that let travellers’ AI agents query availability, prices, and promotions. In this model, the AI agent would be working for and operated by the traveller. In other words, the entry point for travellers is their AI agent (e.g., ChatGPT).

- Agent-to-Traveller: in which autonomous AI agents serve or sell directly to travellers, providing personalized products, services, or recommendations. For example, an OTA creates its own AI agent that curates and offers trips packages tailored to the traveller preferences. In this model, the AI agent will operate under the brand of the OTA. In other words, the entry point for travellers in this model is not their AI agent but the website or app of the merchant (e.g., Expedia).

- Agent-to-Agent: where AI agents independently negotiate, collaborate, or transact with one another, forming a fully automated layer of commerce (e.g., where a buyer's AI agent communicates with a OTA's or supplier's AI agent to autonomously discover products, compare options, negotiate terms, and execute purchases).

At this point in time, the emerging actual use cases of agentic commerce mostly concentrate on Business-to-Agent and Agent-to-Traveller models. In contrast, although the Agent-to-Agent model is expected to have a significant impact in the future, the necessary technology and compliance frameworks are still far from reaching the required level of maturity (e.g., major regulatory changes and company policy updates are still needed).

From an OTA perspective, pursuing the Agent-to-Traveller model, whereby the OTA builds its own AI agent for travellers, would be an opportunity to control its content and the user experience, limiting the risk of replacement. But for this model to be successful, the OTA must develop an AI agent that offers as good user experience as other conversational tools in the market (e.g., ChatGPT, Gemini) – which will require significant investment, in addition to have a large and loyal customer base that favour using the OTA’s AI agent over others.

Nevertheless, the Business-to-Agent model is set to have the most immediate impact for OTAs, with AI companies (e.g., OpenAI, google, Microsoft, Perplexity) actively working with payment providers to enable checkout and payment experiences via their respective conversational AI agents. This article will concentrate in describing the risks and opportunities of introducing the Business-to-Agent model in the existing OTA’s payment flows.

In a Business-to-Agent model, the payment processing of an OTA will fundamentally change in the context of agentic commerce, where AI agents autonomously conduct purchases on behalf of travellers. This transformation is driven by advanced AI-powered autonomous agents, tokenization, and new payment protocols developed by the international payment networks, payment service providers, and fintech companies.

Unlike traditional card-not-present (CNP) transactions where a human buyer initiates and confirms the payment remotely (via the OTA), “person-not-present” transactions push further by removing the human buyer from the immediate checkout process. The AI agent is authorised in advance (e.g., via digital mandates or specific authorisation layers), to make transactions that are secure, auditable, and trusted, even though the actual payer (the human buyer) is absent in that exact moment.

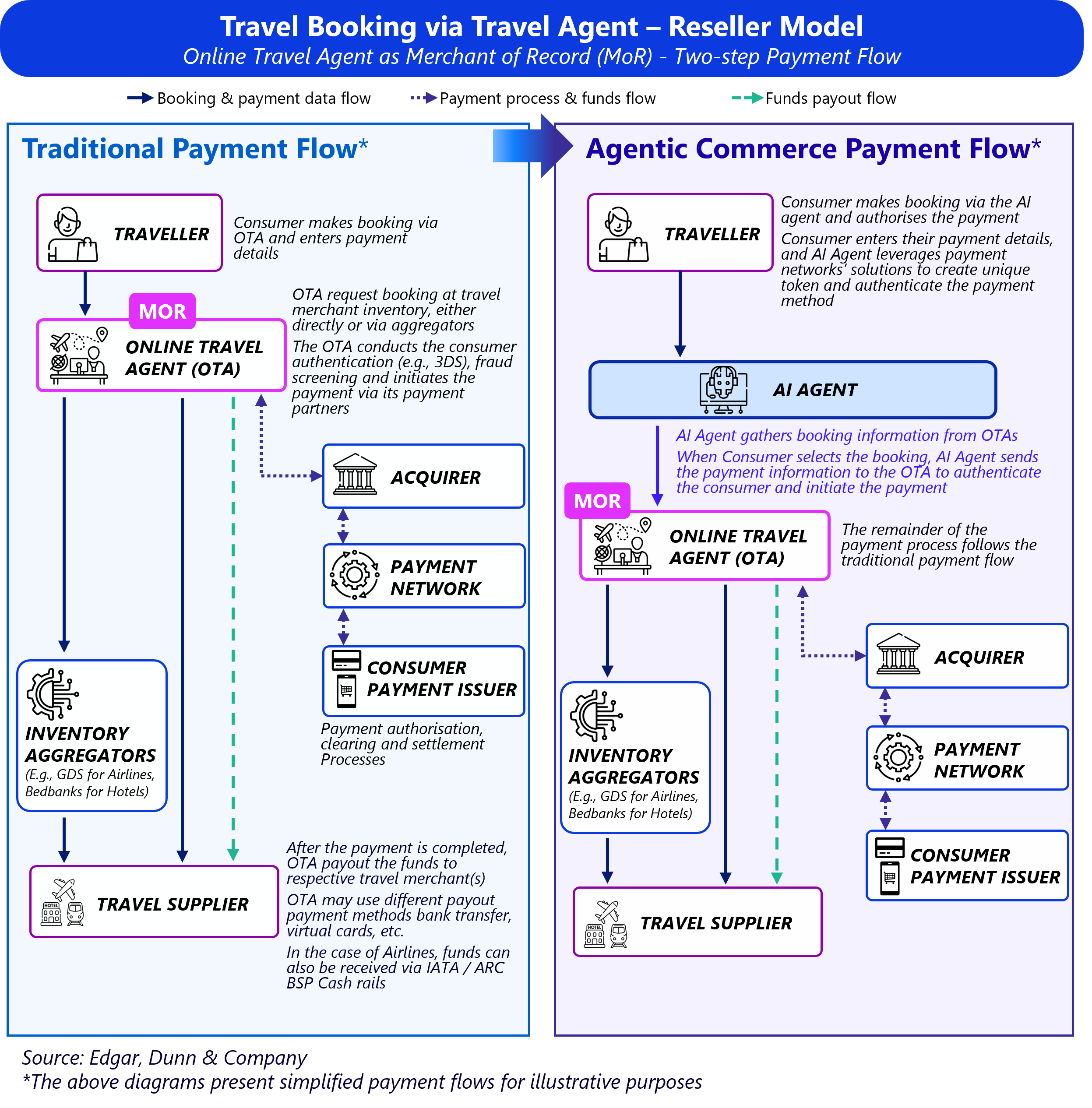

The involvement of the AI agent will vary depending on the payment model, including which player acts as the MoR in the transaction. As already stated, traditionally either the OTA (reseller model) or the travel supplier (pass-through model) are the MoR. But it is also worth considering the possibility of this MoR role shifting to the traveller’s AI agent, either directly or via partners.

Impact on the Reseller Payment Model

The payment flow in the reseller model, when the OTA is the MoR, can be considered as a two-step flow, as the funds go from the traveller to the OTA and then, from the OTA to the travel supplier. The introduction of the agentic Business-to-Agent model will impact the first leg of the payment flow, as the AI agent will play a role between the traveller and the OTA.

In agentic commerce, the OTA will need to first make their booking data available to AI agents via APIs as well as adapt its checkout technology. Once this happens, then the traveller will be able to authorise the payment for the travel booking presented by their AI agent, which will leverage the unique token containing the traveller’s payment information (if previously registered) and then, autonomously work through the checkout process and initiate the payment authentication (3DS, fraud prevention) and authorization processes via the OTA’s payment partners.

In this scenario, despite being the MoR, the OTA will lose control over the entire traveller’s booking and payment experience, which traditionally has been one of the main reasons for the reseller model. As a consequence, from a payment perspective, the OTA may risk missing sales if the payment fails, as the communication to the traveller will be via their AI agent, as well as miss out on additional cost-saving or revenue-generating opportunities like offering alternative payment methods or currency conversion services (e.g., DCC and/or MCP3).

At the same time, opening its content to AI agents would create an additional sales channel for the OTA, while mitigating the risk of those AI agents sourcing the same content from elsewhere as we will see in the pass-through model

Impact on the Pass-through Payment Model

In the pass-through model, the OTA sources the booking information from either the travel supplier directly or via inventory aggregators. Then, at the time of payment, the OTA passes the payment details to the travel supplier directly or indirectly (e.g., IATA / ARC BSP “Card” rail in the airline space), for the travel supplier to conduct the payment as the MoR. Therefore, the OTA plays a pure intermediary role in both, booking information and payment flow.

The introduction of an AI agent is likely to have a considerable effect on the OTA business for this pass-through model compared to the reseller model. In theory, in the pass-through model, the OTA could become another inventory aggregator and therefore, the AI agent could select other sources for the booking information, such as traditional inventory aggregators (e.g., bedbanks, GDSs, or PMS providers) or the travel supplier directly, and then pass the payment information in the same manner, leaving the OTA outside of the equation.

The OTA’s agility in responding to these changes will be a decisive factor. Having a distribution and payment strategy that considers the potential impact of agentic commerce will be essential to mitigate the risks of becoming yet another inventory aggregator or of being by-passed entirely.

OTAs that are trusted and account with a large traveller base, based on loyalty programmes or meeting travellers’ payment expectations will have a stronger position against these risks.

Agentic Commerce Creating New Payment Models

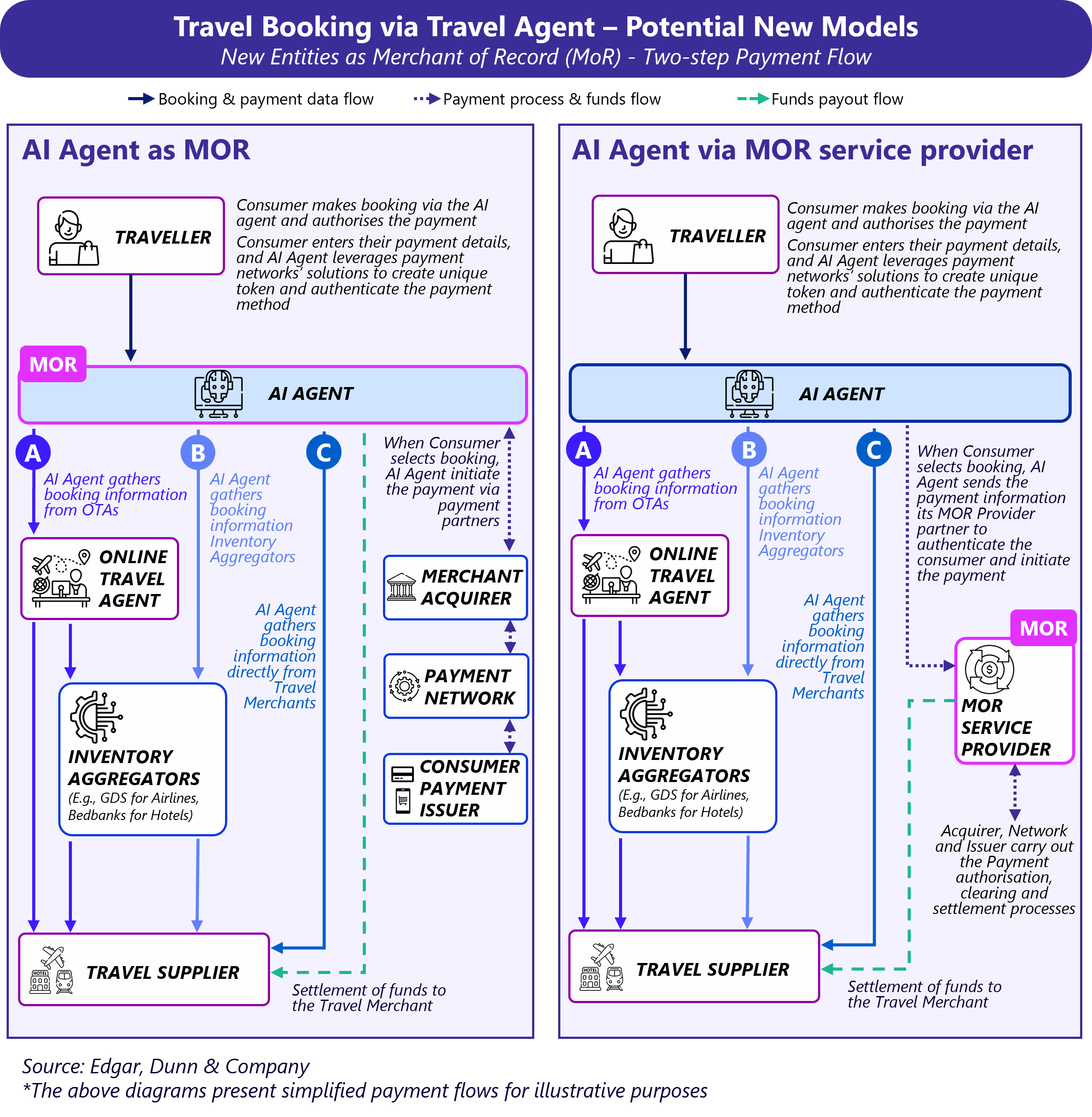

In the travel space, it has been proven that the MoR does not necessarily have to be the end merchant, as the OTA has historically been able to play this role. Therefore, the entry of a new intermediary such as AI agents, begs the question: can the MoR role be taken over by these new players? In theory, the answer is yes.

Taking over the MoR role has significant legal, compliance and operational implications for AI companies, as they would shift from being a pure technology provider (i.e., transferring information only) to a payment intermediary (i.e., moving funds in a two-step payment flow) – see “AI Agent as MOR” diagram below.

The overhead of being the MoR could be transferred to a partner (i.e., “MoR service providers”), that assumes the responsibility for the entire payment process. The AI agents would send the payment information to this partner to conduct the payment authentication and authorisation, as well as to collect the funds and then send the payout to the end travel supplier. – see “AI Agent via MOR service provider” diagram below.

Putting ourselves back in the OTA mindset, if the AI agent becomes the MoR, the risks for the OTA mirror those of the pass-through model: it could end up acting as an inventory aggregator or being by-passed entirely, with the AI agent potentially sourcing the same content from other providers. Conversely, if the AI agent has no interest in becoming the MoR, the OTA could partner with the AI agent and assume the role of MoR service provider itself, effectively operating under the reseller model as described at the start of this article.

What’s Next?

The travel industry is the one of the verticals most accustomed to complex purchasing and payment flows, as intermediaries like OTAs have the option to be the MoR. Additionally, travel suppliers are already familiar with the distinction between reseller and pass-through models. Introducing agentic commerce therefore adds yet another layer of complexity to an already intricate ecosystem. However, for other verticals, where the payment processes are more straightforward, the introduction of agentic commerce will also bring similar complexities depending on who performs the MoR role.

From the OTAs perspective, there are a lot of opportunities and risks with the rise of agentic commerce traffic. It is important to keep in mind that the transformation will be led by traveller behaviour, as travellers will be the ones choosing where to search and pay for their travel bookings. It is essential for OTAs to define their future content distribution and payment strategy thinking of implications of an agentic commerce ecosystem in terms of risks and costs, but also in terms of potential business expansion and revenue creation.

Draw on over two decades of EDC’s proven travel payment expertise, our team specialises in navigating today’s toughest payment challenges, uncovering breakthrough opportunities, and building robust mitigation strategies for tomorrow’s risks. EDC can empower your business to stay ahead of new developments in the travel payments ecosystem: we would be pleased to talk with you if you need help sorting what to do and how to do it in an agentic commerce environment.

1 In the travel industry, the so-called “reseller model” is often referred to as the “merchant model,” as this model involves travellers paying their travel agent (but travel agents do not necessarily purchase and resell products). However, to maintain consistency and avoid confusion with other terms used in this article, we will refer to it as the reseller model.

2 The “pass-through model” is also referred to as the “agency” model.

3 Dynamic Currency Conversion and Multi-Currency Pricing.

The content of this article does not reflect the official opinion of Edgar, Dunn & Company. The information and views expressed in this publication belong solely to the author(s).

Julia is a Manager based in EDC’s Paris office with over 6 years of strategy consulting experience within payments and financial services in several European, North American, Latin American and Middle Eastern markets. She has developed valuable expertise by working with a wide variety of clients across the payments value chain (e.g. central banks, issuers, acquirers, payment schemes, merchants and payment providers) with a larger focus on retail and travel verticals. Julia holds a BSc in Business Management from the Complutense University of Madrid and an MSc in Professional Development from the University of Alcalá. Outside of work, Julia likes to read and plays tag rugby.

%20(1).webp)

%20(1).webp)

.webp)

.webp)