.webp)

Western Union’s ~$500M acquisition of Intermex1 is more than just an expansion of its retail footprint in Latin America and US Hispanic communities. It signals a strategic bet that a dense, trusted network of physical locations can be just as important as digital scale for cross-border remittances.

While companies like Remitly or Wise have successfully scaled through UX optimisation and pricing transparency, Western Union is doubling down on the strategic value of neighbourhood-based distribution. In many migrant-heavy communities, people continue to prefer initiating transfer through retail agents located in grocery stores, convenience stores, standalone remittance shops, and check-cashing outlets. This reality makes distribution networks not a legacy cost but a strategic asset.

Remittance flows and the resilience of cash

In recent years, remittance flows to Latin America and the Caribbean reached roughly $160 billion, with Mexico receiving about $61 billion in 20221. Intermex brings over 6 million active customers2 to Western Union, concentrated in key corridors like US- Mexico, US-Guatemala, US-Honduras, and US-Dominican Republic. A key part of Intermex’s strategic value lies in its agent network embedded in Hispanic grocery stores and neighbourhood retailers serving migrant communities. Locations such as Fiesta Mart or Cardenas Markets act as trusted access points where migrants already shop and send money.

With this acquisition, Western Union’s combined network now includes nearly 100,000 agent locations3, mostly in migrant-dense neighbourhoods in the US and in accessible payout points across Latin America. Corridor density is critical: in high-volume routes like US–Mexico, having many local access points not only strengthens customer trust but also provides operational leverage. It allows providers to manage liquidity, optimise FX spreads, and negotiate more effectively with payout partners.

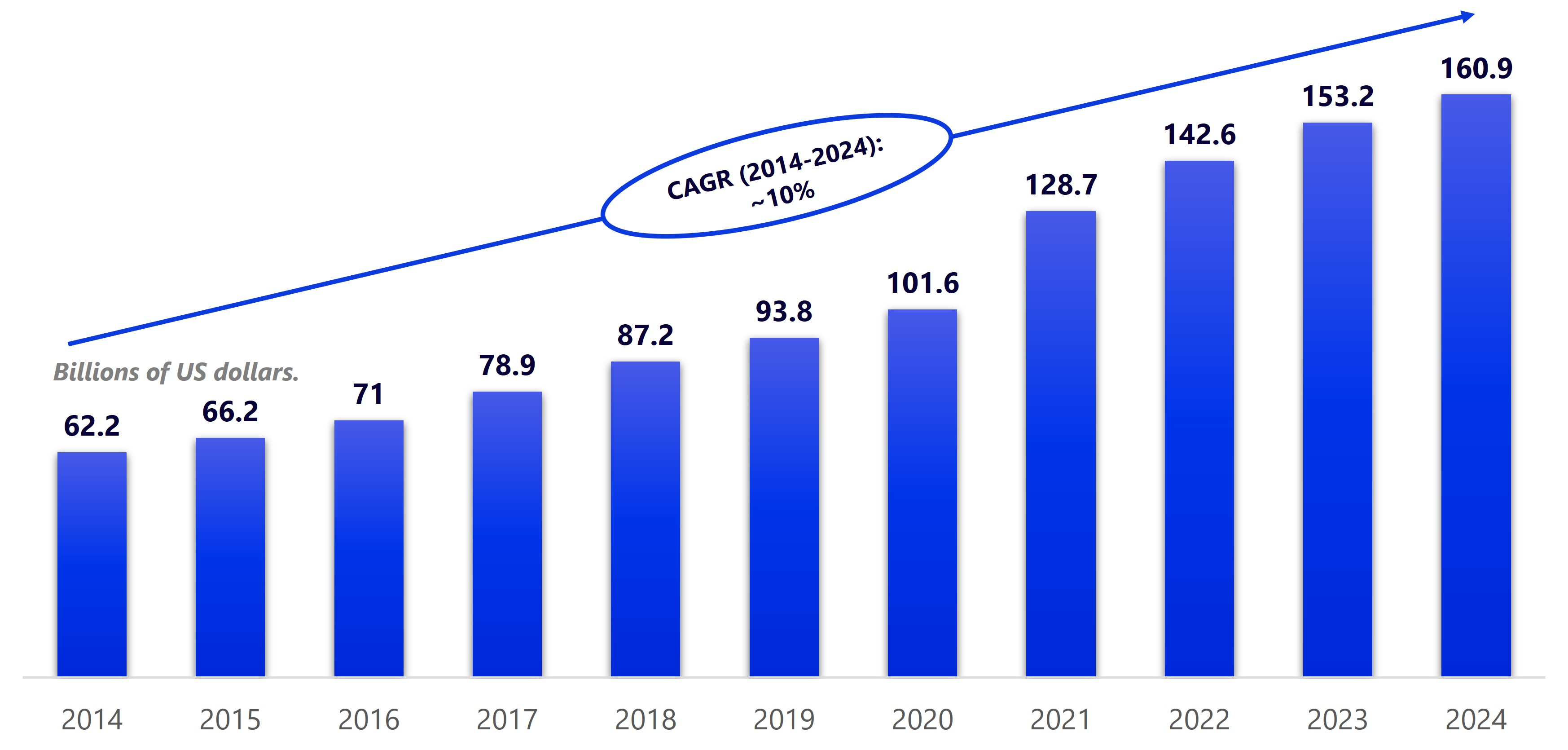

FIGURE 1: Remittances to Latin America and the Caribbean (2014-2024)

In 2024, emigres sent $161 billion to Latin America and the Caribbean in remittances, according to the Inter-American Development Bank's (IDB) calculations.

Source: Inter-American Development Bank - Remittances to Latin America and the Caribbean in 2024, based on data from central banks.

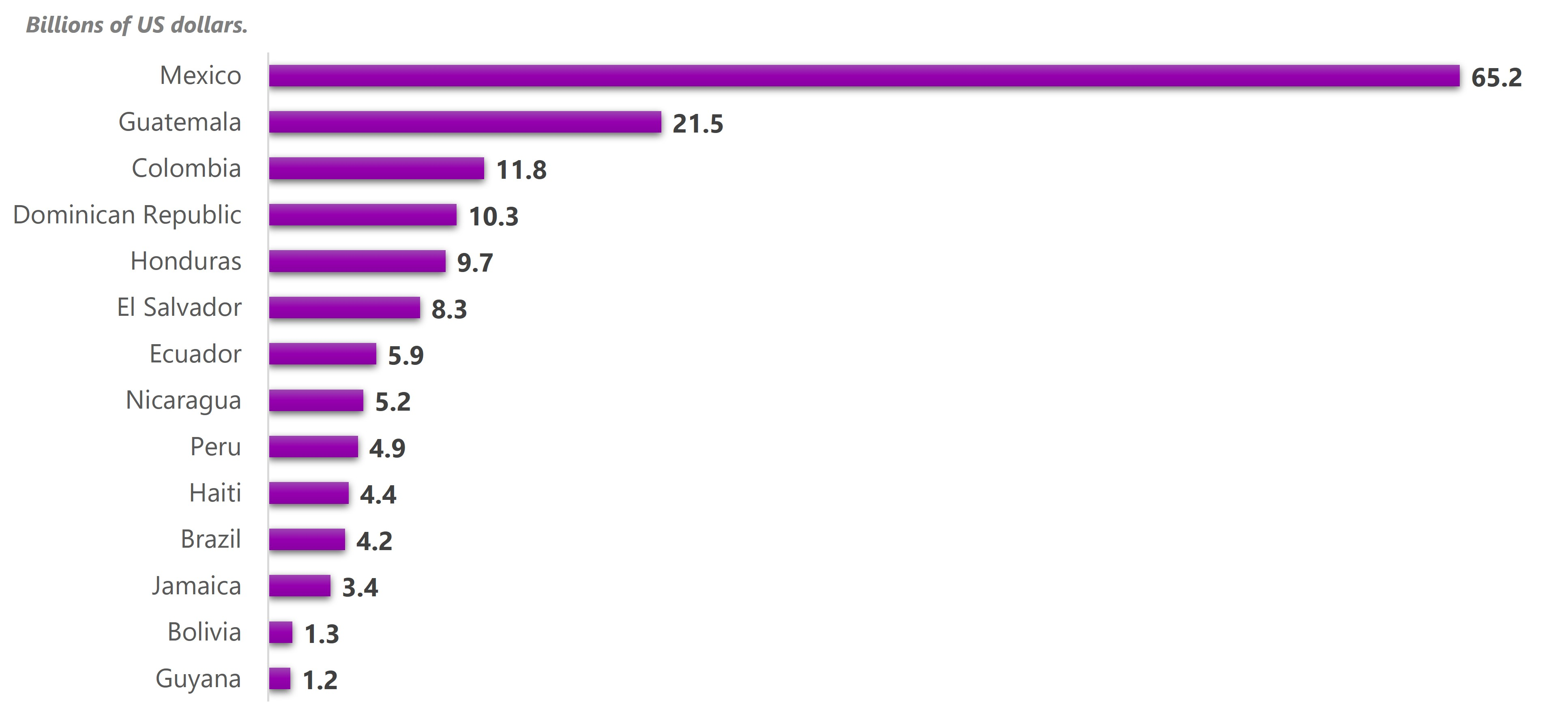

FIGURE 2: Remittances received per country

These are the countries in the region that received more than a billion dollars in remittances in 2024, according to the IDB's estimates:

Source: Inter-American Development Bank - Remittances to Latin America and the Caribbean in 2024.

What Western Union is really buying: corridor control and distribution density

One of the most valuable aspects of this acquisition is its potential to accelerate Western Union’s retail-to-digital strategy. Approximately 28% of Western Union’s digital customers started their relationship with the company through a physical retail location4. Intermex adds millions of customers who rely on in-person cash transactions, particularly in corridors where cash-in behavior remains the norm.

Once this trust is established, introducing digital channels - app-based transfers, A2A (‘Account-to-Account’), card-to-account, or wallet payouts – become easier. This gradual cross-sell is far more cost-effective than traditional digital acquisition channels, which depends heavily on paid marketing and referral incentives to acquire customers online. Physical access, in other words, can be a springboard for digital growth rather than an obstacle.

Why retail still matters: distribution as strategic infrastructure

By combining Western Union’s digital capabilities with Intermex’s agent network, the company now operates a truly omnichannel platform across the Americas. This model integrates:

- Wide-reaching cash-in and cash-out infrastructure

- Robust digital channels (app, web, A2A)

- Extensive bank and wallet payout networks

- Localised corridor-specific promotions and loyalty programs

- Deep community presence through bilingual, community-based agents

For digital-only players, building a comparable retail distribution network would require thousands of local partnerships, extensive agent onboarding and significant compliance oversight, making it costly and slow proposition.

Competitive implications for the remittance industry

Latin American corridors remain among Western Union’s most profitable. With Intermex, the company can:

- Lower cost-to-serve through shared infrastructure

- Gain leverage in negotiations with retail chains and payout partners

- Improve FX and fee management due to higher corridor density

Meanwhile, digital competitors face the opposite challenge: acquiring new customers often requires high marketing spend and promotional incentives, while access to cash-based segments remains limited. In key corridors such as U.S.–Mexico, digital players like Wise and Remitly have intensified price competition, sometimes advertising zero upfront transfer fees and monetising primarily through FX spreads. This dynamic puts pressure on physical networks to justify higher pricing through convenience, trust, and cash access - factors Western Union is clearly betting will remain valuable. By consolidating its footprint where physical distribution is key, Western Union strengthens the parts of its business that are least affected by digital price pressures.

This deal points to a broad shift in the market: hybrid models that combine digital services with strong local networks may outperform digital-only approaches, particularly in corridors where cash remains dominant. For banks and wallets expanding in Latin America, it’s important to note that partnerships and physical access still matter.

Risks and challenges

The integration of two large retail networks is operationally complex and subject to regulatory scrutiny, particularly given tightening AML/KYC requirements across the US and Latin America.

The value of the acquisition also depends on the success of digital migration. If Intermex customers remain largely cash-based, anticipated synergies will take longer to materialise.

Additionally, digital competitors may respond with aggressive corridor-specific pricing to defend their market share.

What industry players should watch next

Over the next 12-24 months, several factors will determine how well Western Union leverages this acquisition:

- The pace at which Intermex customers adopt digital channels

- Expansion of payout networks, including wallets and instant-bank rails

- Changes in corridor pricing

- Consolidation and cost efficiencies among agents

- Additional Money Services Business (‘MSB’) acquisitions that strengthen strategic corridors

In an industry often framed as a story of digital disruption, the Intermex acquisition suggests a different reality: distribution, trust, and corridor expertise remain some of the most durable competitive advantages. The deal also reflects a broader consolidation trend in the remittance industry. For example, WorldRemit’s acquisition of Sendwave in 2021 aimed to expand its presence in key remittance corridors and strengthen its cross-border transfer network. Together, these developments highlight how remittance players are scaling both digitally and through distribution capabilities. More broadly, the transaction signals a shift toward a hybrid model where digital capabilities and physical distribution reinforce each other rather than compete.

Charlotte Piron-Seth, Volker Schloenvoigt and Tue To contributed to this article.

The content of this article does not reflect the official opinion of Edgar, Dunn & Company. The information and views expressed in this publication belong solely to the author(s).

Edgar, Dunn & Company is an independent and global strategy consulting firm specialising in payments and digital financial services. The firm was founded on two fundamental principles of client service: provide deep expertise that enhances clients’ perspectives and deliver actionable advice that enables clients to create measurable, sustainable change in their organisations. Our team is composed of experienced professionals who take a highly pragmatic approach to client issues and deliver analysis that is solidly grounded by experience and know-how. We provide both strategic advice and the business services required to translate that advice into action. Our team is made up of consultants with varied nationalities. We have native speakers covering key markets around the world.

%20(1).webp)

%20(1).webp)