With AI-driven traffic to US retail sites surging 4,700% just over the last year, the Agentic Commerce opportunity is certainly coming to fruition. Edgar, Dunn, & Co forecast that Agentic Commerce will reach $2.9 trillion in retail transaction flows alone by 2030, comprising 29% of total e-Commerce and growing at a 185% CAGR (2026-2030). While this new commerce channel primarily impacts discovery, rather than core payment flows, acquirers cannot afford to be slow to adapt. As adoption progresses, we expect to see a widening bifurcation between acquirers that are ready for Agentic Commerce and those that are not, driven primarily by their readiness to assist and enable their underlying merchants.

What is Agentic Commerce?

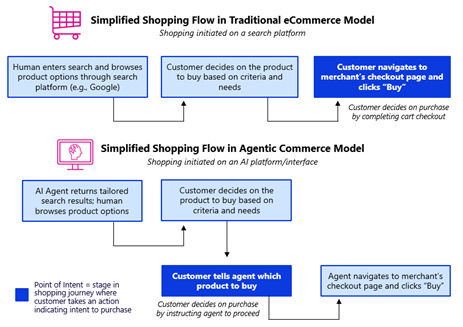

Agentic Commerce is an emerging model of commerce where transactions are being completed with the use of an AI agent or an LLM. Agentic payments are a component of Agentic Commerce, and is defined as the autonomous completion of a payment at checkout by an AI agent. Agentic commerce as we know it today generally excludes the agentic payment piece - an AI agent can complete most of the shopping journey, but still requires a human to verify and authenticate a payment - this is defined as human-in-the-loop Agentic Commerce. The future end state of Agentic Commerce is one where AI Agents autonomously navigate the entire shopping journey, from discovery to payment, on behalf of consumers anticipating needs or wants.

So how does Agentic Commerce work in reality (with human-in-the-loop)? Let us illustrate with an example: a customer looking to book a flight from San Francisco to New York might log onto their preferred AI interface (e.g., ChatGPT). They search “Find me flights from SF to NYC for next week that are $300 or less”. The AI Agent autonomously scans various web pages by accessing merchant APIs and returns a set of matching flights. After the consumer selects their preferred flight, they authorize the payment under a set of defined guardrails, allowing the AI agent to complete the transaction.

We are still in the early days of the Agentic Commerce evolution, and both technical capabilities and regulations are evolving before we will see transactions that are truly autonomous end-to-end. Much of the real-world applications today are more remnant of an embedded checkout within an AI platform (such as ChatGPT Instant Checkout), with significant human-in-the-loop involvement required (i.e., clicking to authorize transaction amount, entering card details, etc.).

As a result, while the surge in AI-driven traffic is significant, near-term economic impact to acquirers is expected to be minimal as the industry progresses past a “proof of concept” stage. This gives acquirers an opportunity to prepare and position themselves over the next 12-24 months to be best situated to benefit from Agentic Commerce.

Agentic Commerce Changes Discovery, Not Core Payments

Fundamentally, Agentic Commerce does not change fundamental processing rules for acquirers, though this does not mean acquirers should remain complacent. Today, clearing and settlement flows in an Agentic Commerce transaction remain largely the same, with transactions continuing to process over existing rails, such as cards. This is largely attributable to early developments by Stripe, who has announced development of one-time use Shared Payment Tokens (SPTs) which tokenizes, vaults, and forwards the agentic payment to the acquirer (using like-for-like issuance of a debit card), ensuring the acquirer receives the transaction in the same tokenized format as it does for a traditional e-commerce transaction. The long-term (10-20 years) future of Agentic Commerce may run on Stablecoin rails and look different from today’s payment flows.

The primary change Agentic Commerce brings to e-commerce is around discovery flows. In an Agentic Commerce transaction, the action of a consumer completing a purchase is shifted from the merchant’s checkout page to the to the point of intent. Discovery and brand differentiation move upstream, with the agent deciding which merchant to fulfill the request with.

Further, Agentic Commerce will transform into a new e-commerce shopping channel, much like mobile commerce did previously. Just as mobile commerce was driven by the ubiquity of smartphones and the introduction of mobile-optimized apps, Agentic Commerce will be propelled forward by growing adoption of AI tools and platforms among both consumers and businesses.

These changes to discovery will create new pressures on merchants as they look to navigate changes introduced by Agentic Commerce, and they will increasingly look to their acquirers and PSPs for help navigating this evolving landscape. Acquirers and PSPs are closely aligned to practical experimentation and may become a “sandbox”. If a company wants to test a bot that purchases autonomously, they’ll look to or partner with their acquirer to build the technical capabilities for that bot to transact securely.

How Acquirers Should Respond Today

Despite the fact that the core payments processing functionality for acquirers does not change significantly, there will still be winners and losers. The merchant acquiring market is likely to diverge, with adaptable and Agentic Commerce-native acquirers/PSPs on one side and legacy providers viewed as slower to innovate on the other end. While some capabilities are better suited to full-stack acquirers and PSPs that sit closer to the merchant checkout layer, all acquirers will play an important role in providing merchants with the tools, education, and services they need to navigate this complex and evolving landscape.

The primary way that all acquirers can respond today is by educating merchants and focusing on merchant preparedness. Merchants are confused and trying to navigate this evolving ecosystem, with many currently in an investigative stage. Acquirers and PSPs can fill this gap by focusing on merchant education and assistance. As merchants typically look towards acquirers/PSPs for assistance with payment acceptance anyways, this is a natural extension of an acquirer/PSP’s core responsibilities and offers a way to both strengthen existing merchant relationships and position themselves as experts on Agentic Commerce. This ensures that when Agentic Commerce reaches broader adoption, merchants will come back to these same acquirers/PSPs.

This need for merchant guidance is amplified by the complexity of emerging Agentic Commerce protocols. Numerous payments-focused protocols from the likes of major players including Visa, Mastercard, Google, and Stripe/OpenAI have already launched, which raises questions for all acquirers/PSPs around which to integrate with (if all or any). The landscape is highly fragmented and protocols are largely complementary, with each targeting a slightly different portion of the stack. As protocols are rapidly changing, it makes sense for acquirers and PSPs to maintain multi-protocol flexibility at this stage rather than committing exclusively to one standard. One approach is for the acquirer/PSP to integrate with multiple protocols and act as a single integration point, enabling merchants to connect once and access all supported protocols via an orchestration layer.

Beyond basic processing, full-stack acquirers/PSPs that operate closer to the merchant’s payment infrastructure are well positioned to help bridge AI-driven workflows and existing payment rails. They can translate agent-initiated transactions into scheme-compliant authorization requests the networks can understand. Those full-stack acquirers and PSPs that control merchant payment APIs can also implement conditional pre-authorization logic which governs whether an agent is authorized to initiate a payment (e.g., 'Only approve if the item is in stock and under $50'). While final authorization rests with the issuer, PSPs and acquirers can help merchants manage agent activity and enforce guardrails upstream.

Forward-Looking Considerations for Acquirers

As Agentic Commerce continues to evolve, it will bring about new challenges, as well as opportunities, for acquirers and PSPs. How acquirers choose to respond will continue to shape their role in this Agentic Commerce ecosystem.

As Agentic Commerce gains adoption merchants will increasingly need granular insights into payments performance by protocol. Today, merchants already A/B test payment performance by acquirer. In the future, it will be common to test payments performance by protocol across acquirers (i.e., which acquirer will give me the best performance for ACP?). This could meaningfully divert volume away from poor performing acquirers, underscoring the importance of acquirers beginning to position themselves as Agentic Commerce-native today.

All acquirers may also need to support new metadata fields. These may include fields that indicate agent identity, delegated consent verification, and transaction traceability. While these metadata fields will likely be defined by the card networks, acquirers will need to ensure they can interpret and process these new data fields, which will help to improve traceability and protect against disputes.

Another key challenge is that all acquirers/PSPs must continue to operate within card network guidelines and regulations, potentially restricting innovation. Within these restrictions, existing fraud systems will need to be adapted to accurately differentiate between legitimate agents and “bad” bots, which may include processing agent IDs and delegated consent verification. Finally, autonomous agents may complete high-frequency microtransactions, putting operational burden on acquirers/PSPs to manage settlement and clearing infrastructure when volume spikes.

For full-stack acquirers, another forward-looking consideration is how unstructured consumer intent data will be stored and interpreted. To protect against liability and fraud, intent data will need to become structured. One possibility is that it could be tokenized alongside tokenized payment credentials, although this is still an emerging technological area. This “intent token” would encode delegated consent, agent authorization, and identity. If this becomes the default mechanism, full-stack acquirers and PSPs would need to decide whether to store the intent token themselves or pass it to the merchant. Internal storage would require development of new secure data storage and system controls.

In summary, Agentic Commerce is set to reshape traditional e-commerce discovery while leaving core transaction flows largely unchanged, introducing both challenges and opportunities for acquirers and PSPs. Although core clearing and settlement flows remain unchanged, acquirers and PSPs will begin to diverge between those well aligned with Agentic Commerce and those that fail to support it or educate merchants. While most Agentic Commerce transactions today retain some element of human-in-the-loop, acquirers and PSPs that act now by educating merchants or preparing internal systems for agent-initiated transactions will be able to strengthen existing merchant relationships and position themselves as Agentic Commerce-native. Balancing near-term readiness with forward-looking experimentation will allow acquirers to maintain the most significant advantage in this evolving ecosystem.

Sources:

VGS, Agent Connect Event

UBS

IXOPAY, Architecting Agentic Payments Webinar

VGS, Agentic Commerce and Payments for Merchants Guide

Mastercard, Scaling Agentic Commerce with Trust

Visa, Visa Introduces Trusted Agent Protocol

The content of this article does not reflect the official opinion of Edgar, Dunn & Company. The information and views expressed in this publication belong solely to the author(s).

Davide is a Manager based in EDC’s San Francisco office. He has more than 4 years of strategy consulting experience within payments and financial service clients across the North American, Asian, European, and African markets. Davide’s expertise spans across multiple EDC practices with a focus on the Retailer, Acquiring, Issuing, M&A, and Advanced Payment practices. Davide graduated with an MEng degree in Biomedical Engineering from Imperial College London. Outside of work Davide is likes to plan exotic travels and enjoys several sports and activities, including football (soccer), skiing, running, and hiking.

%20(1).webp)

%20(1).webp)

.webp)