.webp)

Travel payments have significantly changed in the past few years and this article explores the growth of virtual cards in the travel sector.

Global business travel spending reached $1.3 trillion in 2023 and is projected to approach $2.0 trillion by 2027, according to the Global Business Travel Association - GBTA. Behind this very high number lies a complex web of inter-enterprise payments connecting airlines, hotels, Travel Management Companies (‘TMCs’), and other intermediaries. These B2B payment flows easily exceed $1 trillion annually and remain among the most fragmented (and sometimes inefficient) in the global economy. Inefficiencies can include manual bank transfers (or even cheques or physical cash advance!), delayed settlements, and complex reconciliation processes, therefore leaving significant room for process automation, transparency, and cost optimisation.

Virtual cards have been emerging as one of the ways to address these long-standing inefficiencies and ensure the travel industry’s financial infrastructure benefit from better financial rails. Once used mainly by Online Travel Agencies (‘OTAs’) to pay hotels, they now offer the travel industry a path toward process automation, transparency, and better control in supplier payments.

What makes virtual cards different

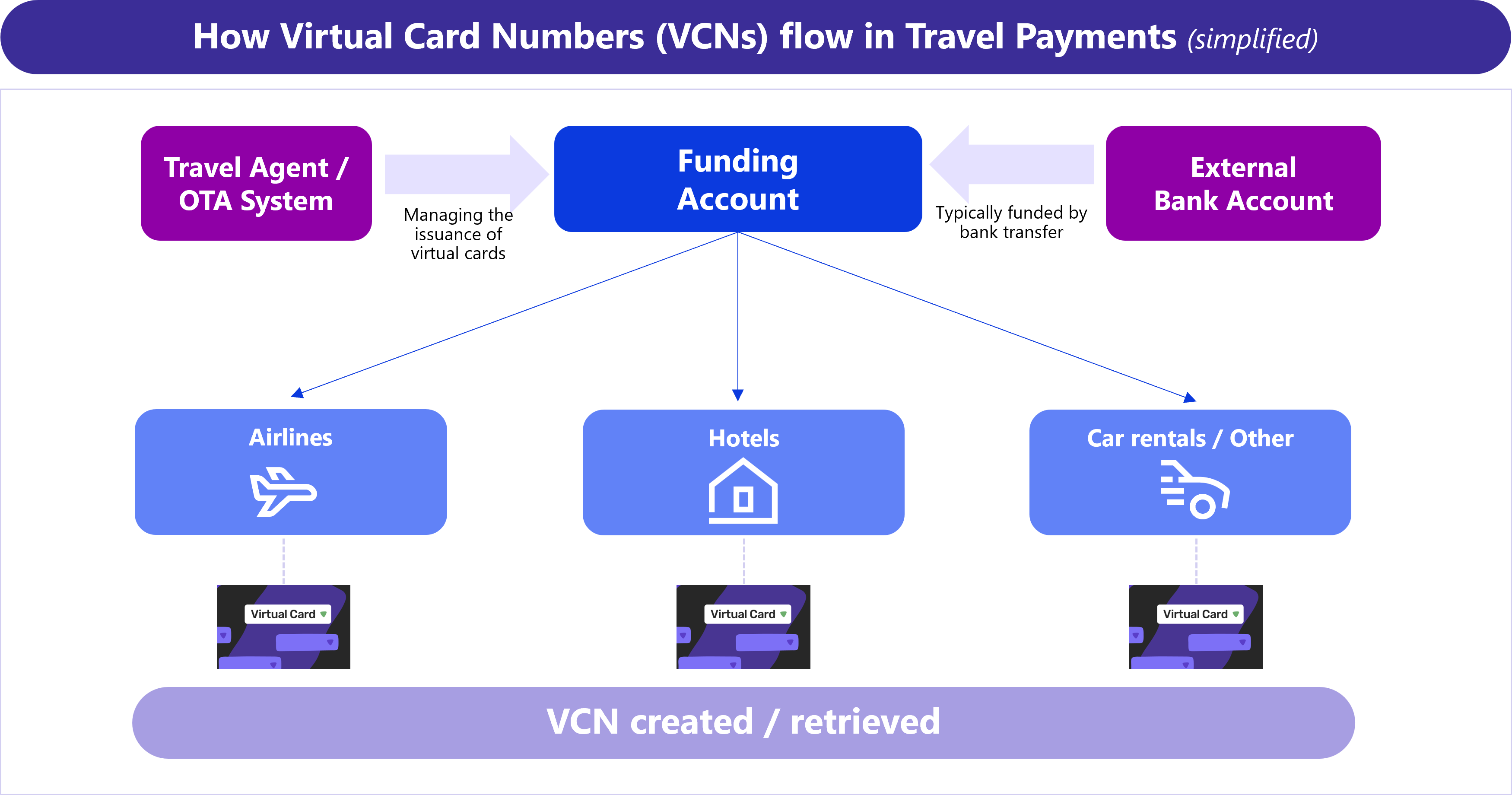

A virtual card is a digitally generated card number (VCN = Virtual Card Number) linked to a central funding account, created for a single supplier, booking, or transaction. Each card number can be configured with unique parameters - spend limit, validity period, currency, or merchant category - and automatically matched with the corresponding invoice or booking reference.

This design makes virtual cards inherently secure, data-rich, and auditable. Unlike personal cards used by travellers or traditional corporate cards, they typically provide Level 3 data and automate reconciliation, VAT recovery, and reporting: three of the largest operational pain points for travel companies.

According to Edgar, Dunn & Company estimates, virtual cards represented 40% of OTA payments to hotels by the end of 20221 reflecting strong momentum in the digitalisation of supplier payments across the travel ecosystem. A study conducted by Amadeus in 2021 among airlines, hotels, and travel agencies found that 74% of airlines identified improved cash flow from shorter settlement cycles as the main benefit of accepting virtual cards. This acceleration mirrors broader B2B payment trends: PYMNTS (2024) observed that virtual cards have moved from niche corporate use cases to mainstream B2B payment solutions, reshaping how companies handle supplier settlement and reconciliation. Meanwhile, Juniper Research (2025) projects that the B2B segment will represent 76% of the global virtual cards market by 2025, increasing to 83% by2029.

The virtual cards value chain in travel

The travel payment ecosystem is unusually complex, involving multiple intermediaries, settlement layers, and legacy processes. Virtual cards simplify and “rewire” this chain by creating a smoother link between four key actors:

- Issuers & program managers (e.g., AirPlus, WEX/eNett, American Express, BNP Paribas, JPMC, Nium) provide the regulated funding, card schemes access, and ensure compliance

- Payment enablers and orchestration providers (e.g., Conferma Pay, Outpayce from Amadeus, HRS) embed virtual cards issuance directly into booking tools, Global Distribution Systems (‘GDSs’), and back-office systems

- Travel intermediaries (e.g., OTAs - Online Travel Agencies, TMCs - Travel Management Companies, aggregators, tour operators) use virtual cards to automate payments to airlines, hotels, and other travel suppliers, with reconciliation often built-in in the product to alleviate specific pain points

- Corporates gain real-time visibility, controls and better reporting, while suppliers receive guaranteed, faster payments

Virtual cards are typically mainly issued by:

- Financial institutions like Bank of America, Barclaycard, BNP Paribas, Citi, HSBC or JP Morgan

- And also by fintech like Adyen, AirPlus, Checkout.com, ConnexPay, Edenred, Fyorin, Nium, Outpayce, Pax2pay, Pliant, Stripe or WEX.

There has been an increasing number of fintechs targeting travel to capture the large value of flows between travel intermediaries and travel providers. Fintechs typically differentiate by a seamless UX, integration with specific actors in travel, high number of currencies and value-added services such as reconciliation or detailed reporting.

Traditional financial institutions are catching up and bridging the gap versus fintech. They have acknowledged the significant opportunity and may often differentiate by offering credit to travel intermediaries.

There is a wide range of virtual card products, depending on their funding (prepaid vs. debit vs. credit), different types of BINs and various economics. Some travel providers such as airlines or hotels may believe they are indirectly paying incentives to travel intermediaries without any consent or transparency. This is the reason why new initiatives are being started by travel providers. In the airline segment, Discover with its product Airline Pay and Nium with its product Nium Airline Payments (NAP) allow airlines to issue directly virtual cards to travel agents.

Nium Airline Payments (NAP) illustrates how the virtual cards model is evolving in practice. Building on the same principles of control, automation and rich data, NAP enables direct travel agency-airline settlement through a closed-loop system aligned with IATA’s Transparency in Payments (TIP), enabling transparent collaboration and sustainable benefits to both participants. Air Europa and Air France-KLM have been among the first airlines to adopt the solution in Europe, signalling how closed-loop and account-to-account settlement systems can complement, rather than replace, virtual cards by extending their logic beyond traditional card rails to provide a seamless process within an ever challenging eco system.

Why adoption is accelerating

Adoption will accelerate further due to four key trends shaping virtual cards in 2026 and further. Travel players are expected to scale issuance via APIs, personalise payment rules, automate reconciliation and strengthen fraud controls according to Modulr.

Several structural forces are driving virtual card adoption across the travel value chain:

- Cash-flow optimisation: suppliers receive funds instantly, improving liquidity

- Risk management: single-use numbers and tokenisation sharply reduce fraud exposure

- Automation & data: automated reconciliation enables accurate cost allocation and VAT recovery

- Commercial alignment: virtual cards create mutual benefits - suppliers receive guaranteed payments and smoother reconciliation, while intermediaries may gain financial incentives

- Regulatory momentum: programmes like IATA Transparency in Payments - TIP, New Distribution Capability - NDC and evolving PSD3 requirements may be catalyst to favour an increase in virtual cards due to transparent, traceable digital payments as well as new flows in the travel industry

- API integration: booking platforms can now issue and match cards automatically within ERP or expense tools

In practice, adoption is also evolving beyond traditional issuance models:

- Liquidity optimisation: some travel agencies now issue virtual cards only at the moment of check-in or consumption, reducing the gap between customer payment and supplier settlement and lowering balance sheet exposure

- Multi-currency issuing: issuing virtual cards in the supplier’s local currency helps travel agencies reduce Foreign Exchange (‘FX’) costs, avoid settlement mismatches and improve acceptance rates, particularly for hotels and low-cost carriers where international payments are required

Remaining barriers to scale

Despite strong momentum, virtual cards remain primarily used in hotel payments and are yet to reach widespread adoption across airlines and the broader supplier ecosystem.

Key hurdles include:

- Fragmented acceptance policies: some airlines still restrict agent-issued virtual cards under Resolution 890 rules. This is often due to the cost of payment acceptance associated with accepting virtual cards: based on our experience, a number of airlines are increasingly migrating away from a binary accept / do not accept policy to a more customised acceptance policy (e.g., acceptance in specific geographies, or in specific channels, or in partnership with specific issuers).The cost of payment acceptance paid by travel providers can hinder the development acceptance network of virtual cards. At Edgar, Dunn & Company, we believe it is key to have a balanced value proposition between travel intermediaries, travel providers and issuers. Virtual cards can bring key benefits to all stakeholders in the value chain and this needs to be discussed and negotiated as part of commercial relationships between the different stakeholders.

- Cross-border FX complexity: costly conversions and settlement mismatches

- Limited education: many smaller Travel Management Companies - TMCs and suppliers remain unaware of benefits

- Interoperability gaps: lack of alignment between GDSs, acquirers, and issuers may slow scalability

Edgar, Dunn & Company works with the whole travel ecosystem and its cooperation with airlines and travel intermediaries shows that supplier onboarding and commercial alignment are some of the critical enablers for the next wave of growth.

Once these acceptance and policy barriers are addressed, the challenge is no longer one of technology availability but the ability to connect and streamline all processes end-to-end. In the United States, for example, 60% of companies have not yet automated virtual cards workflows end-to-end2, meaning that only a minority are fully realising the benefits of real-time issuance, matching and reconciliation. This is where the next competitive advantage will lie: not in issuing virtual cards, but in integrating them at scale into booking flows, ERP systems and supplier processes.

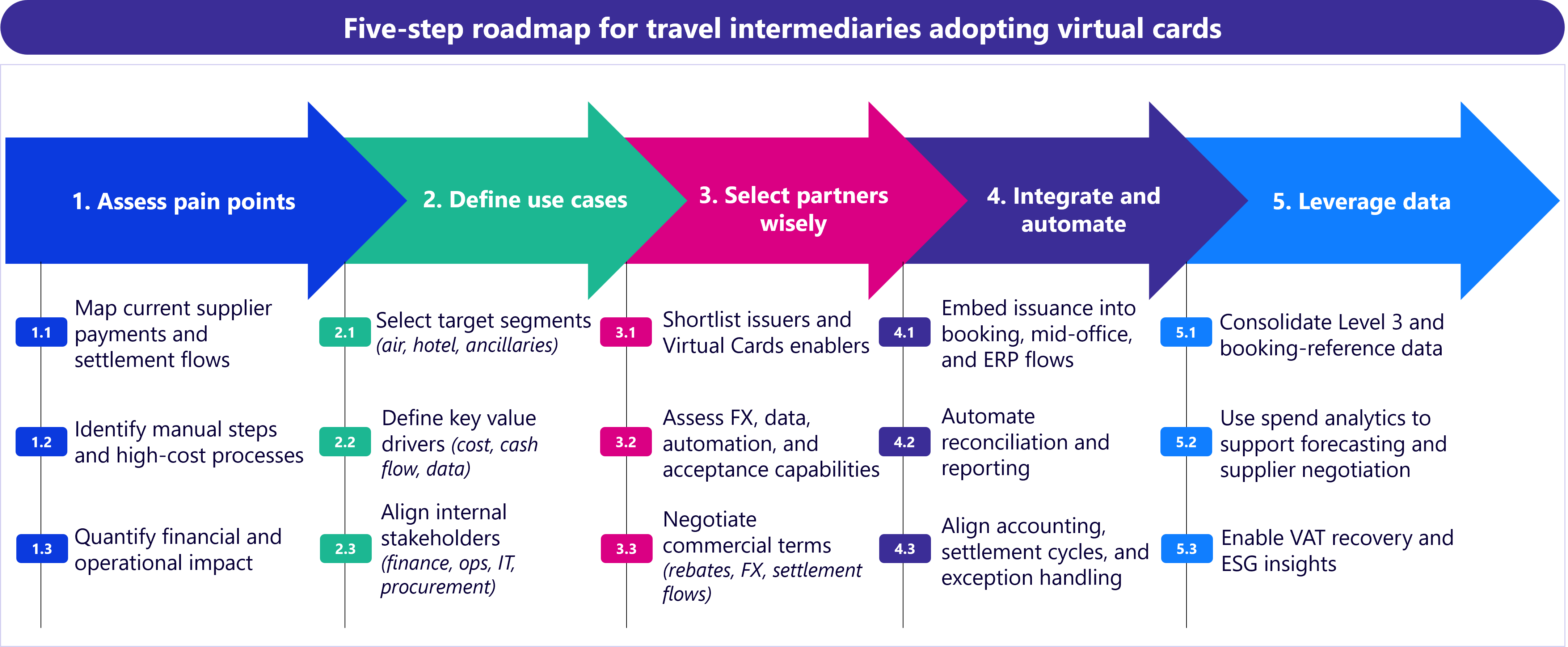

A five-step roadmap for travel players

Drawing on Edgar, Dunn & Company’s experience advising major airlines, issuers, and networks, successful virtual card strategies can follow five key stages for travel intermediaries:

- Assess pain points: map current payment flows andidentify manual or high-cost processes

- Define use cases: select target segments(hotels, air, ancillaries) and key value drivers

- Select partners wisely: evaluate issuers and enablerson FX, data, acceptance, and reporting

- Integrate and automate: embed issuance within booking, ERP, and expense systems

- Leverage data: use granular spend analytics for negotiation, forecasting, and VAT recovery/ESG insights

Travel providers can follow a similar framework to ensure they can successfully launch their own virtual card programme.

The future of B2B travel payments

Virtual cards are moving from tactical tools to strategic infrastructure. As travel volumes continue to increase and regulation pushes for greater transparency, payment flows will increasingly become automated, tokenised, and data driven.

Analysts forecast continued global growth in virtual cards with the total value of transactions expected to exceed $5.2 trillion in 2025 and $17.4trillion by 2029. A key aspect driving this growth is the need to have a balanced value proposition between travel intermediaries and travel providers, and the required negotiation between the different stakeholders.

The question is no longer whether virtual cards will become standard in travel B2B payments, but how quickly stakeholders will negotiate supplier-acceptance and workflow gaps to reach full-scale adoption.

1) Edgar, Dunn &Company, Perspective on Airlines Payments & Virtual Cards, June 2023. Internal analysis based on OTA-hotel transaction data and industry interviews.

2) Virtual Cards in Travel Payments: Four Trends for 2025 - Modulr

The content of this article does not reflect the official opinion of Edgar, Dunn & Company. The information and views expressed in this publication belong solely to the author(s).

This article was originally published for The Paypers.

Charlotte is a Senior Consultant based in Paris. She holds a master’s degree in management (with a finance specialisation) from Kedge Business School, Marseille. Charlotte gained 7 years of experience working as a finance and strategy specialist in France and in India and worked for some of the largest corporates, including Deloitte, L&T Technology Services in Mumbai, Société Générale Corporate & Investment Banking in France, and India. At EDC, Charlotte works on a variety of client projects, from project kick-off through to strategy conceptualisation, with colleagues in San Francisco, Dubai and London. Charlotte loves skiing and enjoys traveling around South Asia.

%20(1).webp)

%20(1).webp)

.webp)

.webp)