.webp)

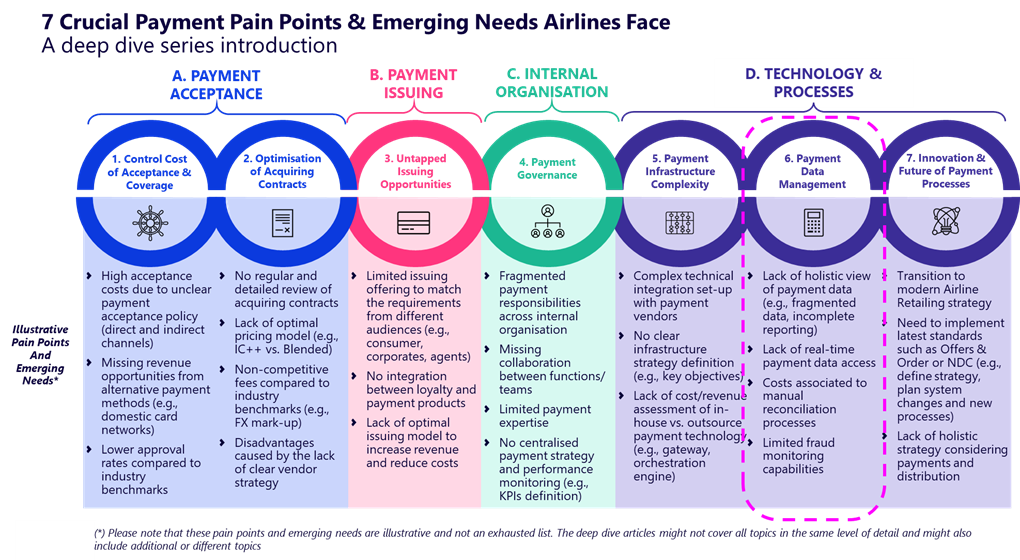

Throughout 2025, Edgar, Dunn & Company (‘EDC’)’s travel payments practice continues to explore the evolving role of payments in the airline industry. Following our discussions on payment acceptance, acquiring contract optimisation, issuing, governance, and infrastructure, this sixth article turns to a crucial enabler behind all these aspects: payment data management.

Focus of this article: Payment Data Management

Airlines handle millions of payment transactions every year across channels, geographies, and partners. And yet, despite this abundance, many still lack a holistic, timely, and actionable view of their payment data. Data remains fragmented across acquirers, gateways, fraud tools, and reconciliation systems, with limited integration. As a result, decision-making is often based on incomplete reporting, and intuition rather than data-based evidence.

In an industry where margins are razor-thin and retail-driven transformation is accelerating, this disconnect poses a critical challenge. Data is the foundation that allows airlines to identify performance gaps, uncover optimisation opportunities, and take truly data-driven decisions.

When payment data becomes a blind spot

Working with airlines worldwide, at EDC, we observe four recurring challenges that limit airlines’ ability to extract value from payment data:

1. Fragmented systems and siloed data ownership: Acquirer reports, Passenger Service Systems (‘PSS’), fraud tools, and refund logs often remain disconnected. Teams working on different systems rarely access a shared view of the data. For example, acquirer reports may not be linked to PSS records, making it difficult to reconcile declined transactions with lost bookings or sales.

2. Lack of cost transparency: Even if airlines are adopting more advanced pricing models like interchange plus plus (IC++), cost transparency remains limited. Many still struggle to obtain detailed, transaction-level reporting from their key partners (e.g., PSPs, acquirers, fraud prevention). Instead, they receive monthly invoices or reports that aggregate fees, with no breakdown of the underlying cost components, preventing granular analysis.

This lack of visibility makes it difficult to track true cost performance, compare providers, or pinpoint areas for optimisation - such as excessive acquiring fees, foreign exchange margins, or unnecessary surcharges. It also complicates reconciliation efforts and limits the ability to enforce SLAs or contractual terms.

For example, EDC worked with a Tier 1 airline that received monthly PDF invoices from one of its acquirers with an IC++ contract - yet without any transaction-level fee breakdown. Without visibility into the interchange, scheme, and acquirer margin components, the airline effectively operates with a “blended” fee view. This defeats the purpose of IC++ pricing transparency and makes it difficult to have an in-depth understanding of payment costs at different levels (e.g., card type, region, or sales channel).

Similarly, another airline supported by EDC faced reconciliation challenges as its acquirer provided only aggregated monthly totals with no details on individual transactions. Finance teams were forced to manually estimate the actual cost per payment method, undermining both accuracy and accountability related to cost control.

In addition to invoices, most acquirers provide Excel-based reports - but these are often still aggregated and lack the granularity needed for reconciliation or detailed cost analysis. While some of the available reporting could be used more effectively, a lack of awareness or technical understanding among those managing payment operations within airlines may limit its value.

As a result, valuable insights remain untapped, and opportunities for optimisation are missed.

3. Manual reconciliation processes: Reconciliation between booking, settlement, refunds and chargebacks is still largely manual, especially for indirect channels. The result is a high operational burden and limited ability to scale. Some airlines report thousands of hours spent annually reconciling providers’ statements with booking platforms and accounting systems.

Recent findings help illustrate the scale:

• In 2024, 52% of Accounts Payable (AP) professionals reported spending more than ten hours per week processing invoices, highlighting the persistent operational burden of manual finance processes.

• Travel-industry research also shows that 44% of travel businesses waste more than 1.5 hours per person, per week on payment inefficiencies, and almost all believe their processes could be much more efficient.

In the airline context, these challenges intensify when combined:

• Airlines often transact through numerous acquirers as evidenced by one major airline working with 16 different acquirers. Each acquirer uses different reconciliation file formats (e.g., xml), requiring bespoke interfaces and making manual ticket-level reconciliation virtually unmanageable.

• Manual reconciliation at this scale can significantly slow month-end close cycles, increase the risk of errors, and consume analyst time that could otherwise support strategic decision-making. It also limits airlines’ ability to conduct a thorough review of revenue accounting and may result in lost revenue.

4. Limited visibility for fraud teams: Fraud rules are often created in isolation, without full transaction context. Without access to behavioral or booking data, fraud systems risk blocking legitimate customers (false positives) or failing to detect suspicious patterns. In a global, high-volume environment, this can directly impact conversion: when genuine customers are wrongly declined, they may abandon the purchase or switch to a competitor. Over time, this also creates reputational risk, as repeat customers or corporate clients may lose trust in the airline’s booking experience and reliability.

What leading airlines are doing right

Some airlines are already turning payment data into a source of competitive advantage. Best-in-class data management includes:

1. Centralised payment architecture: leading carriers consolidate payment data from acquirers, PSPs, fraud tools, and booking platforms. Rather than connecting each internal system directly to external providers, more and more are introducing a payment orchestration layer that acts as a central hub - simplifying integrations, standardising data flows, and enabling unified reporting. This provides a more consistent and accessible foundation for analytics.

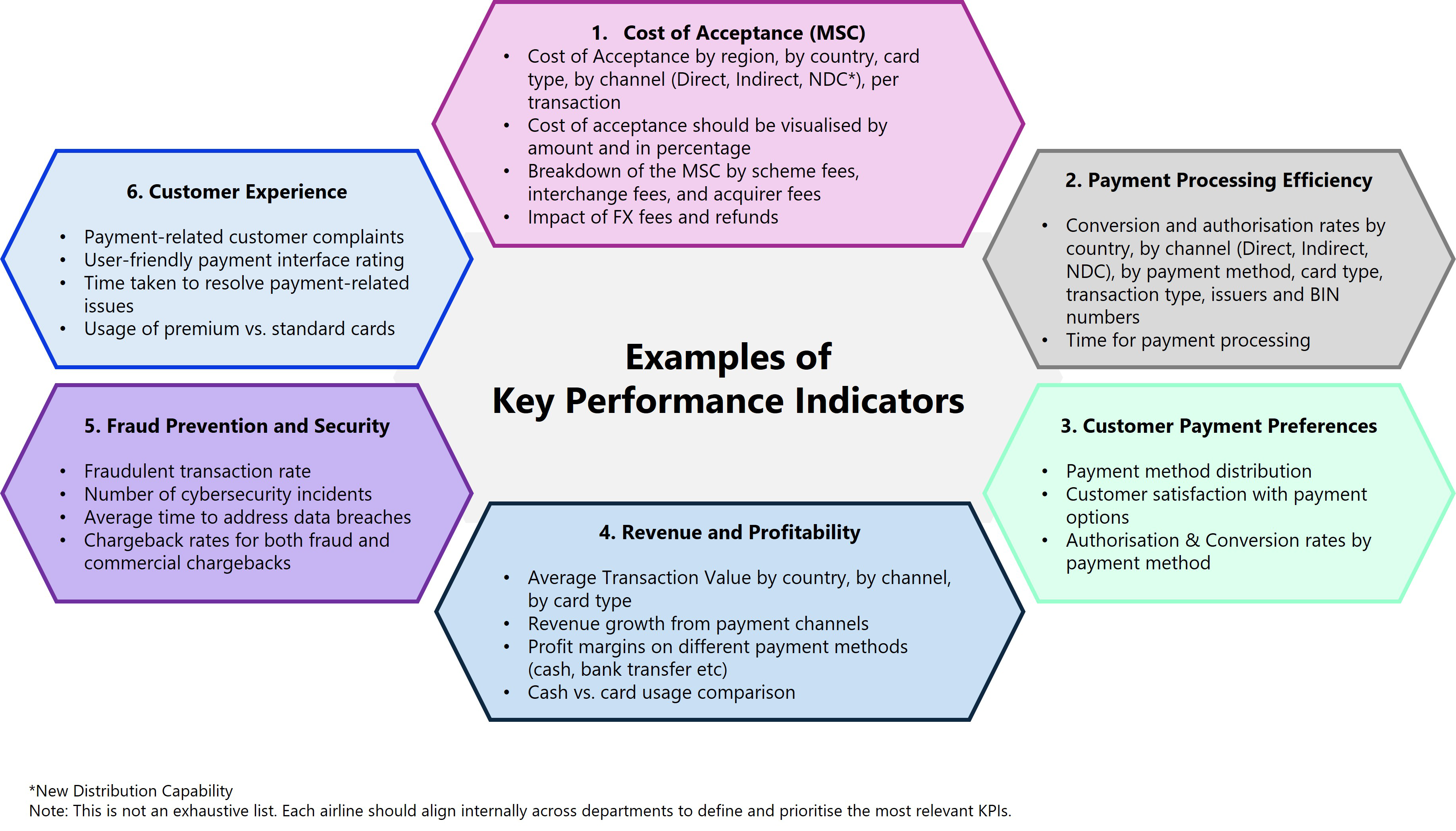

2. Shared KPIs across teams: data is not reserved for finance. Fraud, commercial, and distribution teams all have access to payment dashboards and insights, enabling cross-functional decisions based on a shared understanding of performance.

3. Real-time dashboards: airlines no longer rely solely on monthly reports. Instead, they deploy dashboards tracking key metrics like authorisation rate by issuer, cost per payment method, chargeback trends, and fraud alerts - in near real time.

4. Automated reconciliation: top performers leverage rules-based software to automate reconciliation across channels. Instead of manual matching, exceptions are flagged automatically, freeing teams to focus on resolution rather than reporting.

Data as the payment team’s best ally

Payment data is more than an operational necessity: it is a strategic asset. Airlines that master data management - across both direct and indirect sales channels - are able to:

• Improve conversion: by monitoring issuer-specific approval rates across channels to uncover friction in both direct (e.g., mobile app) and indirect flows (e.g., bookings via Online Travel Agencies (‘OTA’).

According to our global study “Around the World in 80 Ways to Pay”, conducted in partnership with Nuvei in 2023, 74% of travellers would abandon their purchase if their preferred payment method is not available - making payment choice a key driver of conversion.

• Enhance customer experience: by leveraging data to track failed payments, improve customer service, and analyse refund timelines. This also creates an opportunity to offer the payment methods customers prefer across all transaction types (e.g., ticket sales vs ancillaries) and sales channels (e.g., online, in-app, or at the airport).

• Benchmark and negotiate: by comparing the performance of different payment providers per channel to enable more precise SLAs and volume allocations.

• Identify optimisation opportunities: by tracking cost drivers such as high-cost payment methods in certain markets, cross-border interchange, and differences across channels (e.g., OTA vs. direct web), airlines can detect inefficiencies that would otherwise remain hidden.

• Support shorter month-end closing and improve cashflow visibility: by enabling accurate reconciliation across payment methods, acquirers, and sales channels, providing better insight into cash positions and settlement delays.

From strategy to action: 5 steps to build a Payment Intelligence Layer

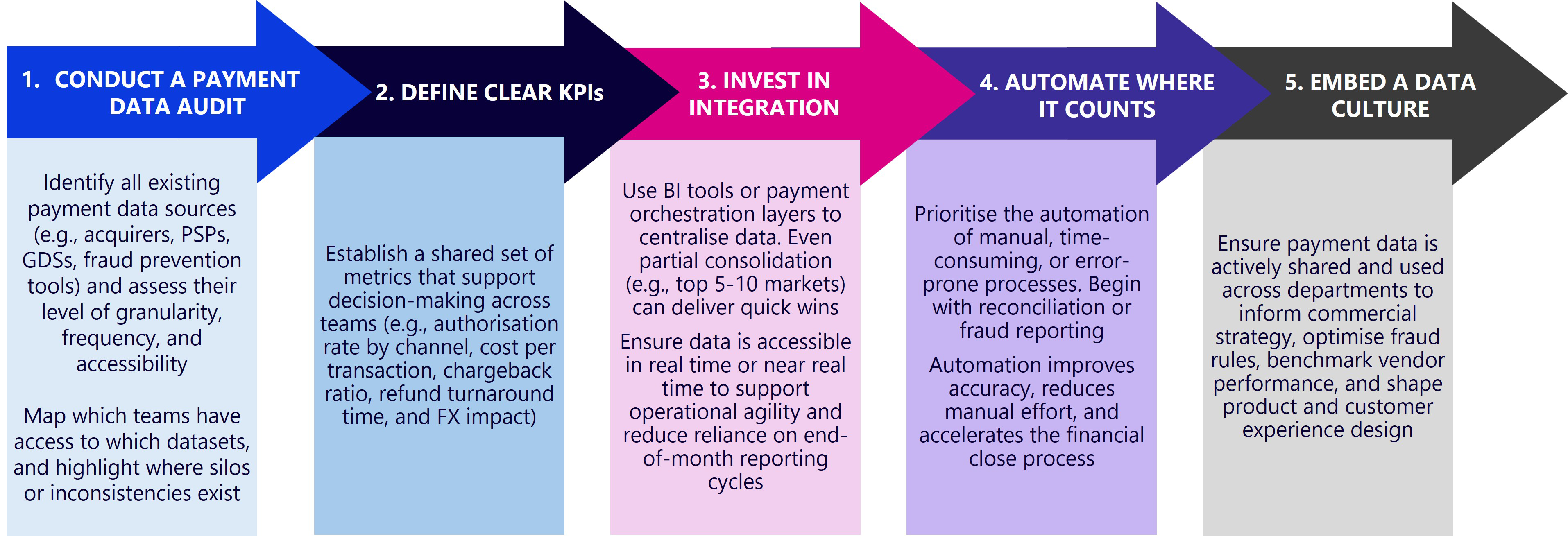

To move from fragmented reporting to strategic value, EDC recommends airlines follow five key steps:

1. Conduct a payment data audit: Identify all existing data sources (acquirers, PSPs, GDSs, fraud prevention tools) and map access and inconsistencies.

2. Define clear KPIs and share across teams: Establish common metrics (e.g., authorisation rate, cost per transaction, refund turnaround) to align decision-making.

3. Invest in integration: Use BI tools or orchestration layers to centralise data and provide real-time or near real-time visibility, starting with the top 5 to 10 markets.

4. Automate where it counts: Prioritise automation of manual, error-prone processes such as reconciliation and fraud reporting to reduce effort and accelerate financial close.

5. Embed a data culture: Ensure data is actively shared and used across departments, organise KPI sessions and CFO-style reporting to drive awareness and informed decisions.

Conclusion: Data visibility as the starting point for Payment Strategy

In a payment strategy, everything starts with data. Without timely, reliable, and unified data, efforts to reduce costs, boost approval rates, and enhance customer experience will remain constrained.

Airlines that invest in payment data management can move from reactive firefighting to proactive strategy. With global travel volumes continuing to grow, the ability to monitor and optimise every transaction will be a key differentiator.

In our final article, we will explore how modern airline retailing - driven by new standards like Offers & Orders and NDC - requires a rethinking of payment processes, systems and strategy, and why bridging the gap between payment and distribution is more critical than ever.

Please reach out to us at travelpayments@edgardunn.com if you want to share your thoughts on our articles or if you want to arrange an introduction call to discuss airline payments opportunities!

The content of this article does not reflect the official opinion of Edgar, Dunn & Company. The information and views expressed in this publication belong solely to the author(s).

Charlotte is a Senior Consultant based in Paris. She holds a master’s degree in management (with a finance specialisation) from Kedge Business School, Marseille. Charlotte gained 7 years of experience working as a finance and strategy specialist in France and in India and worked for some of the largest corporates, including Deloitte, L&T Technology Services in Mumbai, Société Générale Corporate & Investment Banking in France, and India. At EDC, Charlotte works on a variety of client projects, from project kick-off through to strategy conceptualisation, with colleagues in San Francisco, Dubai and London. Charlotte loves skiing and enjoys traveling around South Asia.

%20(1).webp)

%20(1).webp)

.webp)

.webp)