Embedded finance is expanding rapidly as fintechs and digital platforms integrate financial services directly into their core products. The global embedded finance market is projected to grow at a 23% CAGR from 2025 to 2034, reaching $834 billion by 2034, driven by technological advancements and rising demand from both platforms and end-users. On the technology side, advancements in API and modular BaaS capabilities are accelerating adoption. On the demand side, momentum is fueled by revenue pressures on platforms and heightened SME demand for streamlined financial services.

While the early growth of BaaS was primarily enabled by fintechs in the US and Europe, the BaaS ecosystem in these markets has become increasingly crowded, with signs of slowing demand. Furthermore, increased regulatory scrutiny on fintech-bank partnerships has raised barriers for further expansion. For these reasons, future growth will likely be supported by non-financial platforms embedding financial services into existing workflows, forcing banks to modernize and adapt as the competitive landscape evolves.

What is BaaS and What Role Does it Play in Embedded Finance?

Embedded finance refers to financial services integrated and delivered through non-financial businesses. For example, a fintech without a banking license can embed banking capabilities via APIs from a BaaS provider, while non-financial platforms like Uber can partner with a BaaS provider to issue cards to drivers for payouts or expenses. This positions non-financial platforms to create stickier customer relationships and generate new revenue streams. Other members of the value chain also benefit. Fintechs can rapidly launch products with lower upfront costs, and banks can access new customers through lower-cost distribution channels.

BaaS and embedded finance serve distinct roles. BaaS is the back-end regulated banking infrastructure, while embedded finance is the front-end delivery of those services. BaaS solutions are often delivered as white labelled banking services via APIs. BaaS currently contributes to 20% of embedded finance revenue globally, which is largely in line with expectations for an underlying infrastructure layer in a competitive embedded finance market. The remaining 80% consists of services delivered through custom integrations or platform-specific solutions from payments partners (e.g., Shopify Payments via Stripe, Mindbody Capital), which are able to capture a larger share of revenue.

Why BaaS is Gaining Importance

Several structural forces are driving expansion in BaaS adoption, creating a unique inflection point in the market:

· Valuation and revenue pressures: Post‑2022 valuation compression and rising customer acquisition costs have increased pressures on non-financial platforms to diversify revenue streams and differentiate.

· Infrastructure modernization: Historically, collaboration between fintechs and banks required bespoke integrations and custom agreements. Modern BaaS APIs streamline integration capabilities while compliance standards (e.g., KYC/AML) become standardized, reducing integration complexity.

· Data advantages: Higher embedded payments penetration within platforms and improved API infrastructure now allows platforms to better leverage transaction data. This makes embedded financial services easier to launch and scale.

· Growing consumer and SME expectations: Consumers, SMEs, and gig workers demand instant payouts and integrated financial services solutions, often expecting a “one-stop-shop” experience within a single platform.

· Emerging regulatory clarity: Standardized sponsor bank models and improved compliance policies have lowered the barrier for non-financial platforms to partner with BaaS providers, making embedded finance more accessible.

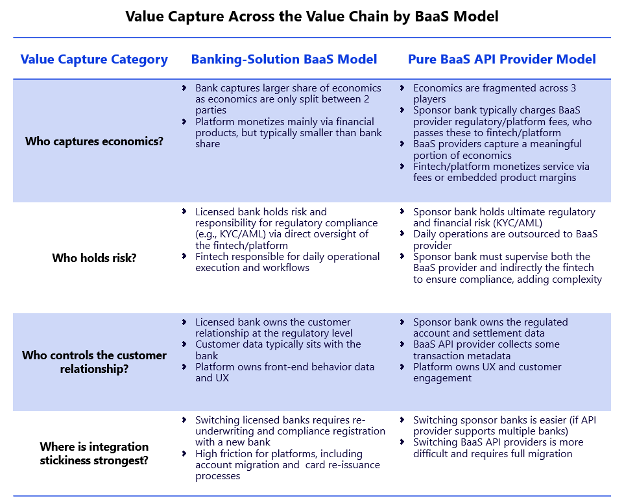

Value Capture Across the BaaS Value Chain

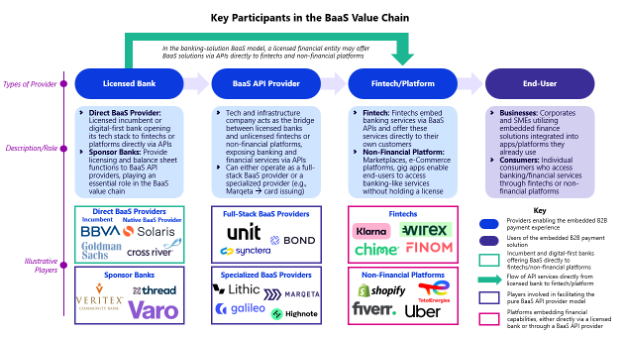

To understand how BaaS enables embedded finance, it is helpful to examine the BaaS value chain in terms of where the banking license and regulatory responsibility sit. In the banking-solution BaaS model, a Direct BaaS Provider (i.e., a licensed bank), either an incumbent (BBVA, Goldman Sachs) or a native BaaS bank (Cross River, Solaris), exposes its regulated banking stack directly to fintechs/platforms via APIs.

Alternatively, in the BaaS API provider model, a sponsor bank provides regulatory licensing to a BaaS API Provider, which acts as middleware connecting to fintechs and platforms via APIs. These providers may operate as full-stack BaaS providers, offering a broad suite of financial services, or specialized BaaS providers, focused on specific capabilities such as card issuing (e.g., Marqeta).

The distribution of economics and value capture differs depending on whether BaaS is delivered directly by a licensed bank or intermediated by an API provider:

Key Challenges to BaaS Growth

While BaaS adoption is gaining momentum, key challenges remain:

· Licensed banks remain legally responsible for partner compliance, including KYC/AML workflows, despite typically having limited control over partner policies. 80% of sponsor banks cite compliance management as a critical challenge.

· Banks and BaaS API providers must manage partner portfolios with varying risk profiles and levels of technical maturity. This increases the risk of compliance errors and inconsistent policy enforcement.

· Legacy banking infrastructure complicates the adoption of modern, API-first technologies and may constrain integration speed and future scalability.

· Margins are compressing. In BaaS API provider models, revenue is split between the fintech/platform, BaaS provider, and sponsor bank, reducing margins compared to a banking-led model. At the same time, increased direct API offerings from banks to platforms creates further pressure on pure BaaS API providers.

How Banks and Fintechs Can Best Position Themselves to Capture Value in an Evolving BaaS Market

In a maturing BaaS ecosystem, most failures typically arise due to unclear relationships between participants. These often stem from misaligned incentives or unclear risk and compliance ownership. Success comes from clearly defining roles and ensuring incentives are aligned across the value chain.

Banks

· Make an explicit positioning choice: Decide whether to operate as a full-stack licensed BaaS provider, offer selective high-margin capabilities (e.g., accounts, payments, lending APIs), or remain a sponsor bank focused on developing partnerships with BaaS API providers.

· Focus on high-value verticals and use cases: Allocate resources to segments where embedded finance is central to workflows (e.g., B2B SaaS, marketplaces, gig platforms) to enhance adoption.

· Invest in API-first infrastructure: Deliver developer-friendly APIs and high uptime to meet fintech and platform expectations.

· Pursue strategic partnerships and M&A: Secure early relationships with fintech or BaaS enablers to accelerate speed-to-market and selectively acquire BaaS capabilities through M&A rather than building entirely in-house.

Fintechs

· Select BaaS partners deliberately: Select between a full-stack BaaS API provider, a specialized BaaS API provider, or direct connection to a licensed bank offering BaaS solutions based on alignment with company size and strategic priorities.

· Focus on vertical-specific products: Tailor embedded finance offerings (e.g., SME lending in invoicing software, gig platform wallets) to the platform to drive adoption and engagement. Expansion beyond core banking solutions drives differentiation.

· Leverage data as a strategic asset: Apply transaction and behavioral data to optimize products and further drive conversion, while maintaining privacy and compliance.

· Continuously iterate: Launch new financial products quickly using modular BaaS APIs and test pricing and product features to respond to end-user preferences.

3 Forces Shaping the Future of the BaaS Market

Looking ahead, three key developments are likely to reshape the structure and economics of the BaaS market:

1. BaaS market will begin to consolidate: The BaaS market is reaching a point of maturity after a period of rapid growth. Over the next several years, it is likely that the currently fragmented market landscape will begin to consolidate as scale becomes increasingly important for sustained profitability and regulatory scrutiny remains high. Synapse, a BaaS provider, filed for bankruptcy in 2024 and was later liquidated due to operational difficulties tracking funds across partner bank accounts and regulatory scrutiny from the CFPB. In this new paradigm, the competitive landscape will be reshaped by strategic acquisitions and partnerships.

2. BaaS API providers to bifurcate between specialized and full-stack providers: As BaaS offerings continue to expand beyond core banking to include lending, treasury, deposits, and insurance, platforms will select BaaS solutions that optimize both integration flexibility and value delivered. We will likely see a bifurcation in the market. Modular, best-in-class capabilities from specialized providers are likely to be utilized by larger platforms, while broader full-stack solutions become geared towards SMEs.

3. Monetization models to shift toward value-based pricing: BaaS monetization is expected to shift from traditional fees toward hybrid and value-based models that align provider incentives with platform scale. Platforms are demanding scalable pricing models, while SMEs exhibit more variable activity patterns. Emerging monetization models include usage-based pricing, which supports fluctuating activity, particularly for SMEs. Performance-based models tie fees to metrics such as transaction volume or customer acquisition.

BaaS has become a foundational enabler of embedded finance, allowing financial services to be seamlessly integrated into non-financial products and workflows. The ecosystem is evolving, with value capture dependent on the BaaS model utilized, though key challenges including regulatory scrutiny, operational complexity, and margin pressure may restrict growth. Banks must decide whether to build or acquire full BaaS capabilities or focus on sponsor-bank roles, while fintechs must select the right partners and deliver embedded solutions that drive end-user adoption and retention.

Interested in discussing BaaS, Embedded Finance, and how these emerging trends could affect your organization?

We would be happy to continue the conversation.

Samee Zafar, CEO

samee.zafar@edgardunn.com

Tue To, Head of Fintech

tue.to@edgardunn.com

Davide Villa, Manager

davide.villa@edgardunn.com

Alex Mueller, Analyst

alexander.mueller@edgardunn.com

Edgar, Dunn & Company is an independent and global strategy consulting firm specialising in payments and digital financial services. The firm was founded on two fundamental principles of client service: provide deep expertise that enhances clients’ perspectives and deliver actionable advice that enables clients to create measurable, sustainable change in their organisations. Our team is composed of experienced professionals who take a highly pragmatic approach to client issues and deliver analysis that is solidly grounded by experience and know-how. We provide both strategic advice and the business services required to translate that advice into action. Our team is made up of consultants with varied nationalities. We have native speakers covering key markets around the world.

%20(1).webp)

%20(1).webp)

.webp)

.webp)