.webp)

Edgar, Dunn & Company, a strategy consultancy specialised in payments with extensive expertise in travel, conducted qualitative interviews with a wide range of travel intermediaries across Europe with global operations, including OTAs, TMCs, bedbanks, NDC aggregators, and tour operators.1,2 Our discussions highlighted a consistent theme: as distribution models evolve, payment complexity is becoming not only an operational issue but also a structural constraint on growth. In this article, we examine the key payment hurdles faced by these players and the trends reshaping B2B travel payments.

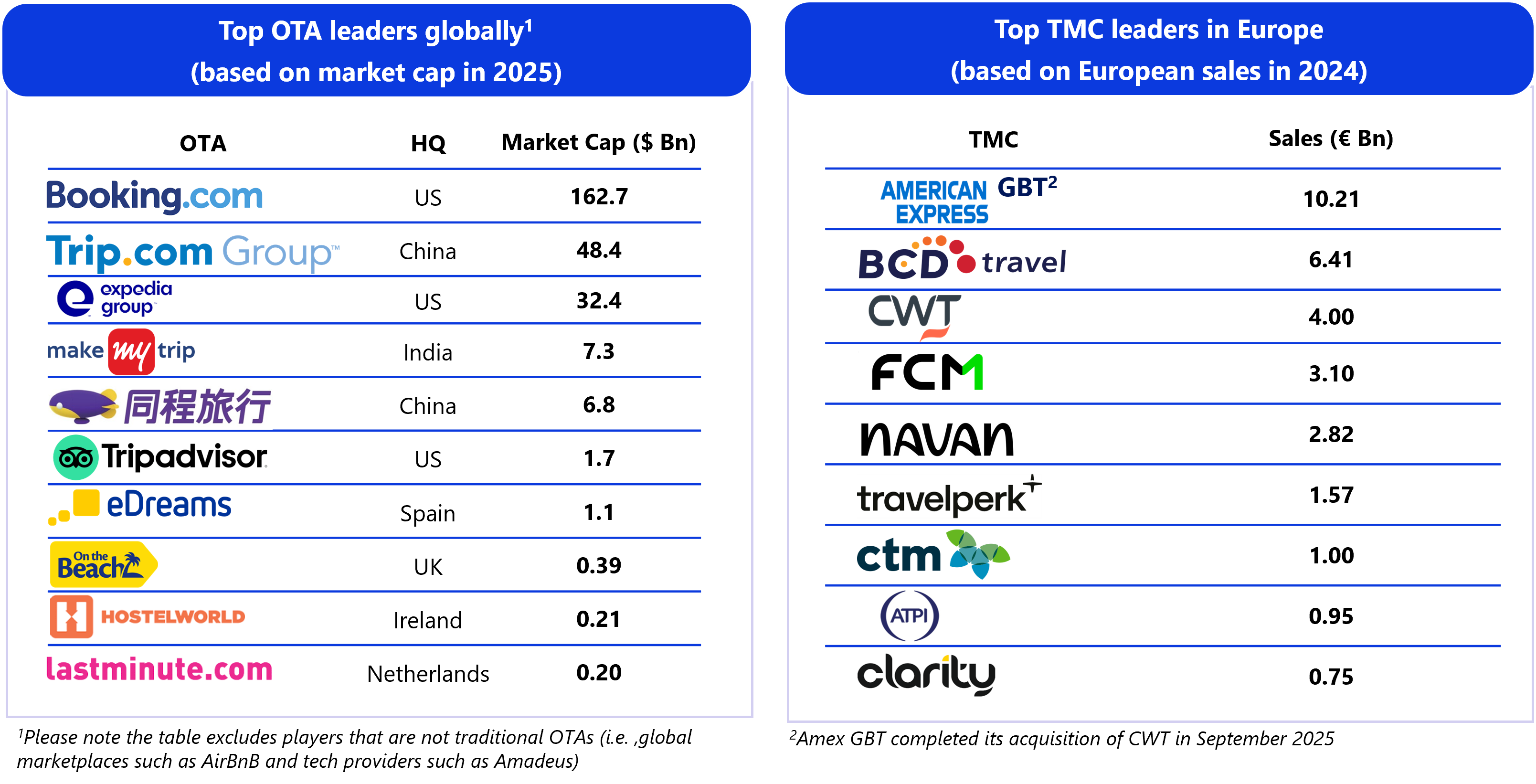

1. Does this sound familiar?

Europe’s online travel market is entering its next phase of expansion, projected to rise from $113 billion in 2026 to $171 billion by 20313. As growth accelerates and distribution models evolve, the travel ecosystem is becoming increasingly fragmented and competitive.

IIn this environment, travel intermediaries face growing operational and financial pressure. Payments, once treated as a back-office necessity, are becoming a strategic differentiator.

Behind every indirect booking lies a layer of invisible B2B payment sophistication. Intermediaries must manage pay-ins and pay-outs, choose between Merchant of Record (MoR) and pass-through models, and support multiple payment methods across many markets. At the same time, emerging distribution models such as agentic commerce and Offers & Orders are reshaping transaction flows and payment strategies. As a result, payment design is no longer just operational. How they fund, route, and settle payments directly influence margins, competitiveness, and supplier relationships. While they absorb many of these challenges, many still lack the integrated tools required to manage it efficiently.

2. Common payments pain points consistently reported by travel intermediaries

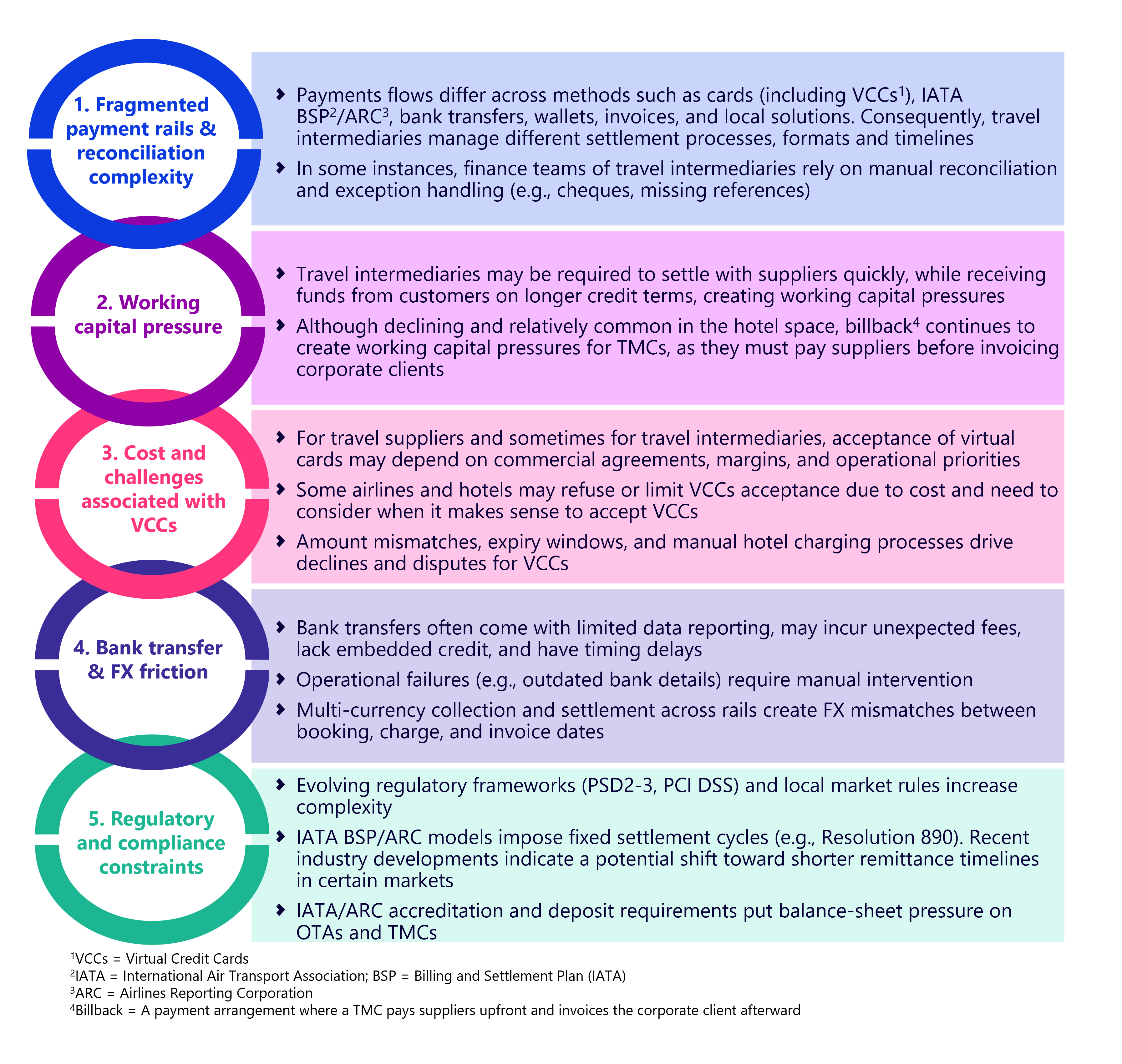

Based on discussions with intermediaries across Europe with global operations, a consistent set of obstacles emerged, reflecting structural inefficiencies in how travel payments are managed today.

They face multiple, connected payment issues that impact efficiency, working capital, and growth. The following five topics highlight the main areas of complexity, from reconciliation and capital pressures to regulatory and cross-border constraints.

2.1. Fragmented payment rails & reconciliation complexity

Reconciliation remains a major operational burden for travel intermediaries, driven by fragmented payment flows across cards, virtual credit cards (VCCs), IATA BSP/ARC Cash, bank transfers, invoice-based settlements, and wallets. Each payment method offers different levels of data quality and visibility, making automated reconciliation difficult. For instance, bank transfers often lack sufficient detail, such as booking or invoice numbers, and may include aggregated monthly totals without transaction-level information, making automatic matching within finance systems difficult. Separately, travel intermediaries must reconcile financial incentives from suppliers and partners, which frequently arrive separately and in inconsistent formats, thus requiring manual matching and exception handling. The lack of standardisation across providers, suppliers, and markets further amplifies the challenge.

As intermediaries scale globally, reconciliation becomes increasingly challenging, spanning multiple systems, currencies, and partners. This results in higher operational costs and growing pressure to improve automation and end-to-end payment visibility.

Addressing this challenge requires greater standardisation of payment data and the adoption of integrated reconciliation and reporting tools that provide end-to-end visibility across pay-in and pay-out flows.

2.2. Working capital pressure

Cashflow management is one of the most fundamental structural challenges for travel intermediaries, driven by timing mismatches between incoming and outgoing payments. Supplier settlement obligations, such as airline BSP remittance cycles or hotel settlements via VCC, are typically fixed and strictly enforced. Meanwhile, many players, particularly TMCs, receive funds later because they serve corporate clients on invoice or credit terms. This creates sustained working-capital pressure, as intermediaries must bridge the gap between supplier payments and customer collections. Billback arrangements, especially in the hotel space, and extended client payment terms can further widen this gap, increasing liquidity risk and balance sheet exposure. As intermediaries scale across suppliers, markets, and volumes, these structural cashflow constraints tie up capital and reduce financial flexibility. Ultimately, they limit the ability to grow efficiently.

Addressing these pressures requires more flexible settlement and funding structures that better align incoming and outgoing cashflows. For example, solutions that combine efficient and affordable payment rails with embedded credit or deferred settlement mechanisms could help intermediaries bridge timing gaps and alleviate cashflow pressure.

2.3. Pain points associated with different payment methods (VCCs, bank transfer)

Choosing the right payment method presents challenges as it requires constant trade-offs between cost, acceptance, and cashflow flexibility, both when collecting and remitting funds.

Virtual cards have become a widely used tool for travel supplier remittance, offering intermediaries financial incentives, strong spend control, enhanced security, and simplified reconciliation, among other benefits. However, their higher acceptance costs, compared with traditional card payments or bank transfers, are typically borne by suppliers such as airlines and hotels, which can lead to limitations or restrictions. Some suppliers may limit or refuse VCC acceptance, while others, particularly hotels, impose operational constraints on when and how cards can be charged. This can result in declines due to activation windows, amount mismatches caused by taxes or local fees, and manual handling at the front desk. In some cases, they may also incur similar costs when receiving payments via virtual cards from partners or clients. Intermediaries and travel suppliers are encouraged to engage in discussions to identify common ground for appropriate VCC usage.

Bank transfers, though cheaper to accept, introduce different limitations. They typically lack embedded credit, reducing cashflow flexibility, and offer limited remittance data, increasing reconciliation effort. Unlike cards, they also do not provide financial incentives.

As a result, the choice and acceptance of payment methods have become both strategic and commercial decisions. Progressively, travel suppliers view how they are settled as part of the overall business relationship, with appropriate-cost payment options often translating into better contractual terms.

2.4. Regulatory and compliance constraints

When operating across multiple markets, travel intermediaries face a highly fragmented and constantly evolving regulatory landscape. Invoicing, tax, and reporting requirements vary significantly by country, forcing them to adapt processes to local rules.

For example, under IATA’s BSP, one mechanism through which travel intermediaries remit funds to airlines, settlement timelines are defined centrally. These timelines can be short and may tighten in certain markets, potentially shifting from bi-weekly to weekly or even shorter cycles.5 This would require intermediaries to transfer funds to airlines quicker, increasing working-capital pressure.6

At the same time, the rollout of mandatory electronic invoicing and near-real-time reporting in several European markets, including France, Germany, Italy, and Spain, adds further operational complications.

Intermediaries must also comply with PCI DSS requirements, KYC/KYB regulations, and industry-specific accreditations such as IATA BSP participation, which require them to provide financial bank guarantees. These obligations create both operational and financial burdens, particularly for players expanding into new or highly regulated markets.

Consequently, compliance is no longer a static back-office function; it has become an ongoing operational capability that directly impacts scalability, market access, and the ability to operate efficiently across borders.

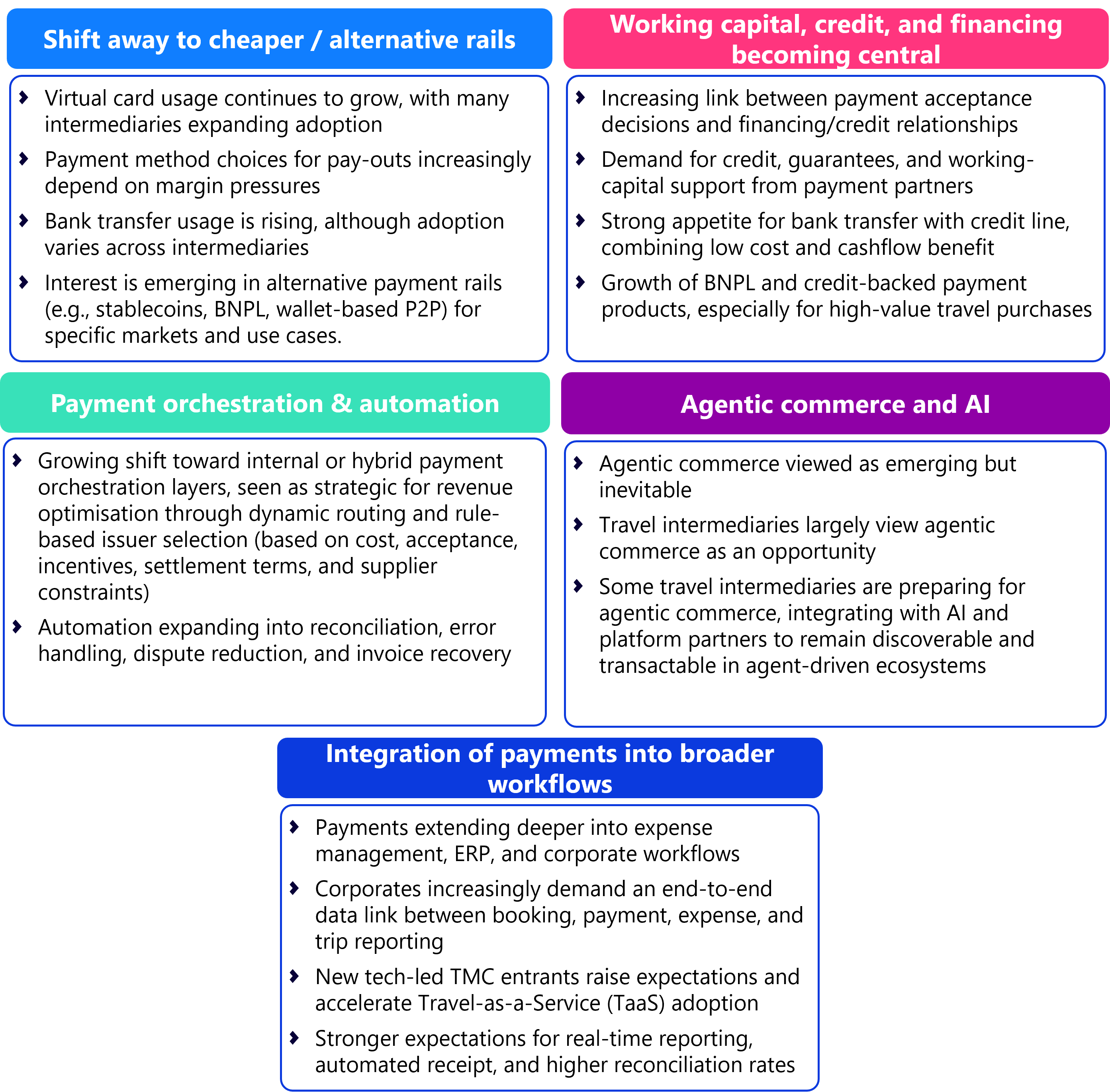

3. The trends shaping what comes next

The travel payments landscape is evolving rapidly, driven by cost pressures, new distribution models, and changing commercial dynamics.

Changes in travel distribution are reshaping payment requirements. The expansion of NDC, growing reliance on APIs, and the rise of agentic commerce are introducing more dynamic, automated transaction flows. Payments must now support increasingly complex interactions among travel intermediaries, suppliers, and platforms, often in real-time and across multiple markets. This evolution is pushing intermediaries to modernise their payment infrastructure to remain relevant in the distribution chain.

For example, agentic commerce introduces new demands around payment integration, identity verification, and settlement, as transactions may be initiated and completed autonomously within digital ecosystems. Many intermediaries are already preparing by ensuring their platforms and payment capabilities are discoverable, transactable, and trusted within these agent-driven environments.

Payments are also becoming more directly tied to commercial outcomes. How intermediaries pay suppliers increasingly affects pricing, margins, contract terms, and access to inventory. In response, many are investing in orchestration capabilities to optimise payment routing and settlement. As a result, payment strategy is becoming a defining factor in their financial efficiency, competitiveness, and long-term scalability.

Finally, tech-led new entrants, especially TMCs, with fully integrated booking, payment, and expense solutions are raising expectations. They increase competitive pressure on intermediaries to modernise payment infrastructure and deliver more efficient financial workflows.

4. A more holistic way to think about travel payments

The key question for travel intermediaries is no longer just how to process payments, but how their payment strategy can facilitate commercial bilateral discussions with suppliers while supporting sustainable margins and growth.

Managing payments effectively requires a deliberate approach to controlling risk, cashflow, and operational burden. This means moving beyond one-size-fits-all models and adopting flexible strategies that can support different suppliers, markets, and commercial arrangements. It also involves engaging with partners who understand the specific realities of travel and maintaining the ability to adapt as regulations, supplier expectations, and distribution models evolve.

In a rapidly changing ecosystem, payments are far more than infrastructure. They are a core enabler of growth, competitiveness, and long-term success.

Do not hesitate to contact us at Edgar, Dunn & Company for support with your payments strategy and to leverage it as a key driver of your future growth.

Research methodology:

The article, written by Edgar, Dunn & Company, is based on extensive qualitative discussions conducted between Q3-Q4 2025 and Q1 2026 with travel intermediaries across Europe with global operations. The sample comprised a range of players, including OTAs, TMCs, bedbanks, NDC aggregators, and tour operators, guided by a consistent interview framework. These interviews examined both pay-in and pay-out flows, covering how they collect funds from customers (corporates) and partners, as well as how they settle with suppliers.

Discussions focused on how they currently manage pay-ins and pay-outs, the structural pain points they encounter, and the emerging needs and trends reshaping travel payments. Conversations were held with senior stakeholders across finance, payments, treasury, and operations functions, providing a comprehensive perspective on both strategic priorities and operational realities.

1 Online Travel Agents (OTAs), Travel Management Companies (TMCs), New Distribution Capability (NDC)

2 Please refer to the end of the article for a detailed overview of the research methodology

4 https://shorturl.at/oNjqS; https://shorturl.at/MSIa7; https://shorturl.at/fskej

6 https://tinyurl.com/48ez3rmh

The content of this article does not reflect the official opinion of Edgar, Dunn & Company. The information and views expressed in this publication belong solely to the author(s).

Edgar, Dunn & Company is an independent and global strategy consulting firm specialising in payments and digital financial services. The firm was founded on two fundamental principles of client service: provide deep expertise that enhances clients’ perspectives and deliver actionable advice that enables clients to create measurable, sustainable change in their organisations. Our team is composed of experienced professionals who take a highly pragmatic approach to client issues and deliver analysis that is solidly grounded by experience and know-how. We provide both strategic advice and the business services required to translate that advice into action. Our team is made up of consultants with varied nationalities. We have native speakers covering key markets around the world.

%20(1).webp)

%20(1).webp)

.webp)