.webp)

The rapid rise of mobile commerce challenges merchants to keep pace with the evolving digital marketplace and consumer expectations. Analysis by EDC highlights a clear trend: mobile commerce adoption continues to grow at a strong pace, with a 19.2% global increase in m-commerce forecasted sales between 2019 and 2029.

M-commerce refers to transactions made via mobile devices such as smartphones and tablets through mobile-optimised apps or websites. This article explores key drivers of m-commerce growth, such as demographic trends and the rise of agentic commerce. It also outlines how EDC’s proprietary 360⁰ payments diagnostic can help merchants and retailers optimise their m-commerce platforms in a harmonised fashion relative to other sales channels.

Mobile Commerce Adoption is Expected to Continue Growing

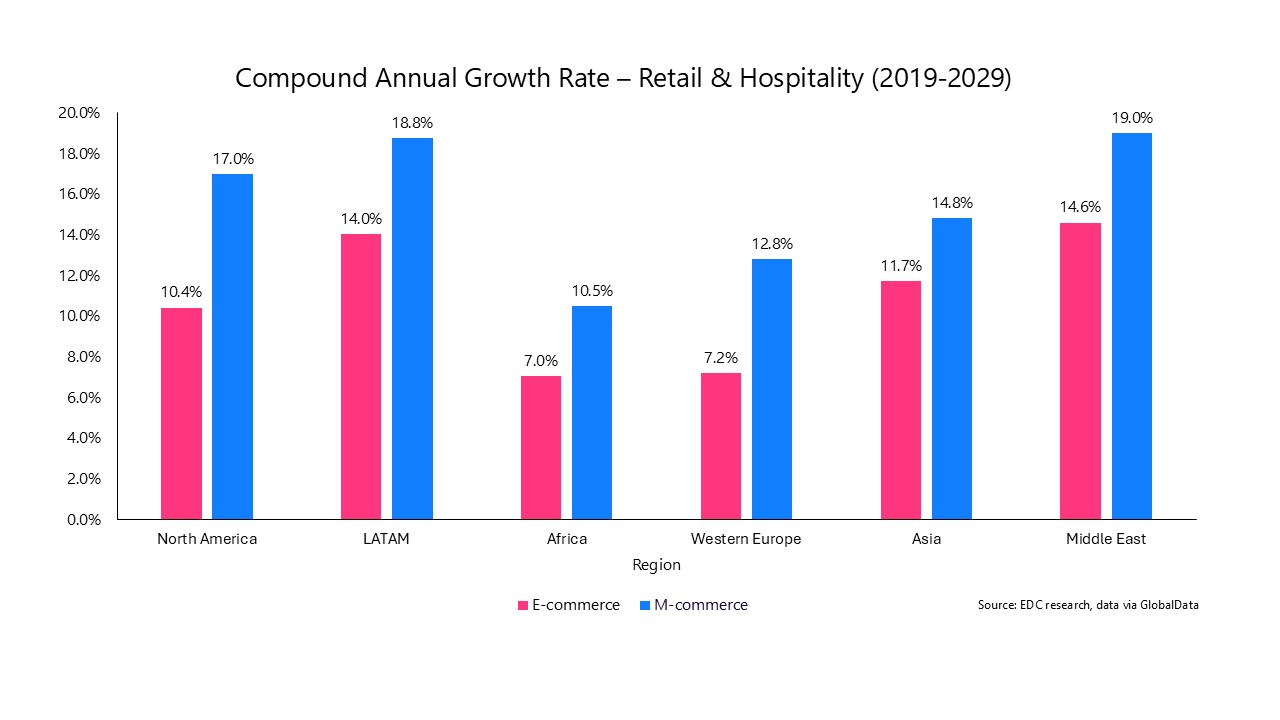

Mobile commerce growth in retail and hospitality is set to rise globally, according to EDC research. As illustrated in Figure 1.0 below, analysis shows that between 2019 and 2029, m-commerce sales are projected to outpace e-commerce growth, with increases of 20.3% in North America, 21.1% in LATAM, 21.3% in Africa, 17% in Western Europe, 16.1% in Asia, and 20.6% in the Middle East. Although baseline m-commerce adoption remains higher in less technologically developed regions, the overall accelerating integration of m-commerce underscores a universal imperative for mobile strategy.

Highlighted in Figure 2.0 below, the Middle East and Latin America experienced the largest annual growth rate over the 10-year period, recording compounding annual growth rates (CAGRs) of 19.0% and 18.8% respectively. Variations in adoption are influenced by socioeconomic, cultural, and infrastructure-related factors as well as overall technological accessibility. With most consumers in LATAM owning smartphones rather than desktops, the region has seen a significant shift toward mobile-first digital transactions, accelerating m-commerce expansion. Asia’s large investment in digital payment ecosystems, including mobile wallets, QR code payments and super-apps such as Alipay, has accelerated the integration of advanced payment systems within the m-commerce ecosystem. In the Middle East, a digitally engaged population, combined with high mobile phone penetration, has driven strong m-commerce growth. Although Africa’s CAGR trails other regions, it holds the largest overall m-commerce share at 79% of e-commerce by 2029. While mobile phone penetration rates are lower compared to developed markets, mobile devices often serve as the primary means of internet access. In contrast, growth in the US and Western Europe has been more incremental, reflecting already mature e-commerce markets that had high baseline activity before the surge of mobile devices.

Do Mobile Commerce Customers Have a Preference Between App and Website Purchases?

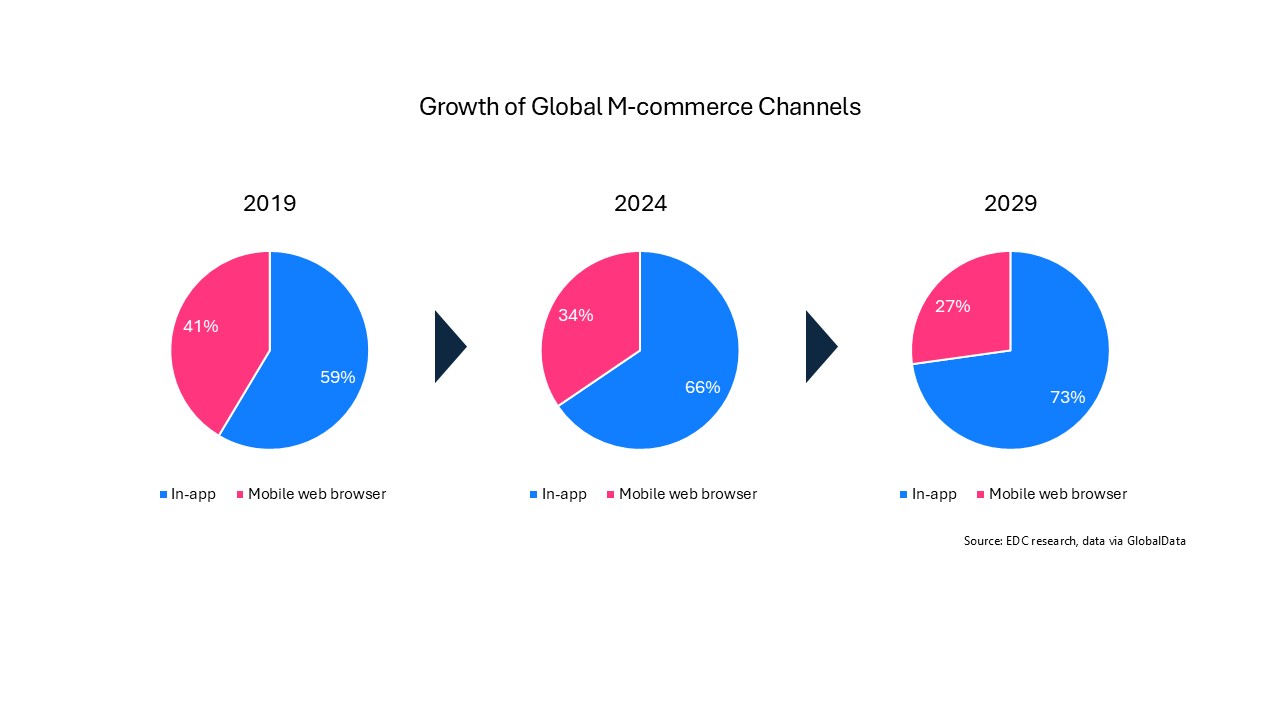

Figure 3.0 shows the growing dominance of in-app payments as the preferred purchasing method in m-commerce. In-app payments refer to purchases made directly inside dedicated branded retail apps, whereas mobile web payments occur via browsers.

There are many possible reasons for this shift in consumer behaviour, driven by convenience and flexibility - reducing friction decreases customer churn and minimises shopping cart abandonment. While most of the features on dedicated brand apps can be somewhat replicated on their web browser equivalents, the overall user experience differs.

By contrast, in-app systems can directly access stored user profiles and purchase history data, while web browsers face increasing limitations on cookie usage and data tracking. This implies that even if the checkout process is fast, it tends to be less personalised, which may hinder conversion. Furthermore, because in-app systems can access user data, payment credentials, and preferences, they provide an ideal environment for agentic commerce. The fragmented, permission-limited nature of mobile web browser payments may make it harder for autonomous AI agents to operate across platforms.

Payment information that is securely stored in the wallet, making checkout almost instantaneous for any app transaction is also an important requirement. Apple Pay and Google Pay are preferred by consumers for in-app payments primarily due to their convenience, speed, and enhanced security. These mobile wallet services allow users to make purchases without manually entering card details or retrieving their physical cards; instead, payments are completed with a simple biometric authentication, such as facial recognition or fingerprint scanning. Apple Pay and Google Pay use tokenisation, meaning the actual card number is never shared with merchants, reducing the risk of data theft.

Integral to the in-app commerce landscape is the evolving role of social media platforms as digital storefronts. Since the mid-2010s, Facebook’s introduction of Marketplace and the launch of Instagram’s business tools have transformed the platforms from traditional marketing channels into seamless shopping experiences. Features such as in-app checkout, product tagging, and shoppable posts have allowed businesses to turn engagement and content into viable sales opportunities. This integration complements dedicated brand apps by expanding reach and discovery. TikTok’s more recent entry, TikTok Shop, showcases the rapid evolution of social commerce, as viewers can purchase products within videos or live streams on their feed. In the space of a few years, the social media digital storefront concept has advanced from the social sharing of product to a fully integrated in-app purchasing experience.

How Agentic Commerce is Changing the Game

Agentic commerce uses AI agents to manage and execute purchases autonomously, delivering personalised shopping experiences. These AI-powered agents can independently research products, compare prices, and finalise the purchase transaction.

Leading platforms such as Shopify have already integrated AI shopping agents within their mobile apps, using transactional APIs and retrieval-augmented generation (RAGs) to deliver seamless customer experiences. Routine tasks can be further automated through greater data integration and access to real-time data analytics. Adobe reported a huge surge in AI-driven buying behaviours, with US retailers experiencing a 1200% increase in traffic originating from AI-generated interactions between July 2024 and February 2025. The surge represents growth from a modest base of AI-driven visits, which initially accounted for only a small fraction of total retail website traffic. This trend is expected to accelerate as platforms enhance features such as API-enabled transactions and more integration, allowing AI agents to enter merchants via dedicated API channels.

Agentic commerce extends beyond retail platforms; payment networks like Visa are actively embracing this shift, developing new protocols and security frameworks that enable AI agents to initiate and safely complete transactions on behalf of consumers. This move is redefining the payment experience by making it possible for AI agents to browse, buy, and authorise payments autonomously. In April 2025, Visa announced its Intelligent Commerce platform, a system that enables AI agents to discover, select, and purchase products on behalf of users. By combining APIs, real-time transaction controls, and agent-specific tokens, Visa enables merchants to integrate agentic commerce into their broader mobile optimisation strategies. The initiative demonstrates how agentic commerce can curate a frictionless, personalised, and secure shopping experience.

Neglecting to develop proprietary AI-driven customer experiences could erode brand loyalty, reduce customer engagement, and increase reliance on third-party AI providers. Hence, merchants must define a strategy to develop their own agents or increase visibility on third-party AI platforms to remain competitive in this rapidly evolving landscape.

Leveraging the 360⁰ Payment Diagnostic for Mobile Optimisation

To fully realise the opportunities presented by evolving m- and e-commerce, merchants can leverage proprietary advisory tools such as EDC’s 360⁰ Payment Diagnostic. The Payment Diagnostic offers a holistic assessment of payment strategies across every touchpoint, helping organisations to identify cost efficiencies, enhance user experience, and select the optimal mix of payment solutions for each channel. Merchants that can harmonise their mobile journeys with other digital channels will ensure mobile commerce becomes a high-performing element of an organisation’s broader omnichannel strategy.

The content of this article does not reflect the official opinion of Edgar, Dunn & Company. The information and views expressed in this publication belong solely to the author(s).

Mark is a Director in the London office and heads up the Retailer & Hospitality Payments Practice for EDC. He has over 25 years of experience of consulting strategy in the payments and fintech industries. Mark works with leading global merchants, and payment suppliers to retailers and hospitality merchants, to develop omnichannel acceptance strategies. He uses the 360° Payment Diagnostic methodology developed by EDC to identify cost efficiencies and new growth opportunities for retailers and hospitality merchants by defining an appropriate mix of payment methods, acceptance channels, innovative consumer touchpoints, and optimizing Payment Service Providers and acquiring relationships. Outside the payments and fintech industry Mark is a passionate snowboarder.

%20(1).webp)

%20(1).webp)

.webp)